fun with 𝔸𝕊𝕋𝕊𝔸 🎈🎈🎈

◀ current CRAN version

![]() ◀ current GitHub version

◀ current GitHub version

We’ll demonstrate some of the capabilities of astsa … the NEWS page has additional installation information.

Remember to load astsa at the start of a session…

library(astsa)

it’s more than just data … it’s a palindrome

⭐⭐⭐⭐⭐⭐⭐⭐⭐

📢 Note: When you are in a code block below, you can copy the contents of the block by moving your mouse to the upper right corner and clicking on the copy icon ( ⧉ ).

Table of Contents

- 1. Data

- 2. Plotting

- 3. Correlations

- 4. ARIMA

- 5. Spectral Analysis

- 6. Detecting Structural Breaks

- 7. Testing for Linearity

- 8. State Space Models and Kalman Filtering

- 9. EM Algorithm and Missing Data

- 10. Bayesian Techniques

- 11. Stochastic Volatility Models

- 12. Arithmetic

- 13. The Spectral Envelope

1. Data

💡 There are lots of fun data sets included in astsa. Here’s a list obtained by issuing the command

data(package = "astsa")

And you can get more information on any individual set using the help() command, e.g.

help(cardox) or ?cardox

| Name | Title |

|---|---|

| BCJ | Daily Returns of Three Banks |

| EBV | Entire Epstein-Barr Virus (EBV) Nucleotide Sequence |

| ENSO | El Niño - Southern Oscillation Index |

| EQ5 | Seismic Trace of Earthquake number 5 |

| EQcount | Earthquake Counts |

| EXP6 | Seismic Trace of Explosion number 6 |

| GDP (GDP23) | Quarterly U.S. GDP - updated to 2023 |

| GNP (GNP23) | Quarterly U.S. GNP - updated to 2023 |

| HCT | Hematocrit Levels |

| Hare | Snowshoe Hare |

| Lynx | Canadian Lynx (not the same as R dataset lynx ) |

| MEI | Multivariate ENSO Index (version 1) 1950 - 2019 |

| MEI2 | Multivariate ENSO Index (version 2) 1979 - 2025 |

| PLT | Platelet Levels |

| USpop / USpop20 | U.S. Population - 1900 to 2010 / 2020 (2 different files) |

| UnempRate | U.S. Unemployment Rate |

| WBC | White Blood Cell Levels |

| ar1miss | AR with Missing Values |

| arf | Simulated ARFIMA |

| beamd | Infrasonic Signal from a Nuclear Explosion |

| birth | U.S. Monthly Live Births |

| blood | Daily Blood Work with Missing Values |

| bnrf1ebv | Nucleotide sequence - BNRF1 Epstein-Barr |

| bnrf1hvs | Nucleotide sequence - BNRF1 of Herpesvirus saimiri |

| cardox | Monthly Carbon Dioxide Levels at Mauna Loa |

| chicken | Monthly price of a pound of chicken |

| climhyd | Lake Shasta inflow data |

| cmort | Cardiovascular Mortality from the LA Pollution study |

| cpg | Hard Drive Cost per GB |

| djia | Dow Jones Industrial Average |

| econ5 | Five Quarterly Economic Series |

| eqexp | Earthquake and Explosion Series — the map |

| flu | Monthly pneumonia and influenza deaths in the U.S., 1968 to 1978. |

| fmri | fMRI - complete data set |

| fmri1 | fMRI Data Used in Chapter 1 |

| gas | Gas Prices |

| gdp | Quarterly U.S. GDP |

| gnp | Quarterly U.S. GNP |

| gtemp.month | Monthly global average surface temperatures by year |

| gtemp_both | Global mean land and open ocean temperature deviations, 1850-2023 |

| gtemp_land | Global mean land temperature deviations, 1850-2023 |

| gtemp_ocean | Global mean ocean temperature deviations, 1850-2023 |

| hor | Hawaiian occupancy rates |

| jj | Johnson and Johnson Quarterly Earnings Per Share |

| lap | LA Pollution-Mortality Study |

| lap.xts | LA Pollution-Mortality Study Daily Observations |

| lead | Leading Indicator |

| nyse | Returns of the New York Stock Exchange |

| oil | Crude oil, WTI spot price FOB |

| part | Particulate levels from the LA pollution study |

| polio | Poliomyelitis cases in US |

| prodn | Monthly Federal Reserve Board Production Index |

| qinfl | Quarterly Inflation |

| qintr | Quarterly Interest Rate |

| rec | Recruitment (number of new fish index) |

| sales | Sales |

| salmon | Monthly export price of salmon |

| salt | Salt Profiles |

| saltemp | Temperature Profiles |

| sleep1 | Sleep State and Movement Data - Group 1 |

| sleep2 | Sleep State and Movement Data - Group 2 |

| so2 | SO2 levels from the LA pollution study |

| soi | Southern Oscillation Index |

| soiltemp | Spatial Grid of Surface Soil Temperatures |

| sp500.gr | Returns of the S&P 500 |

| sp500w | Weekly Growth Rate of the Standard and Poor’s 500 |

| speech | Speech Recording |

| star | Variable Star |

| sunspotz | Biannual Sunspot Numbers |

| tempr | Temperatures from the LA pollution study |

| unemp | U.S. Unemployment |

| varve | Annual Varve Series |

{kind=link}

2. Plotting

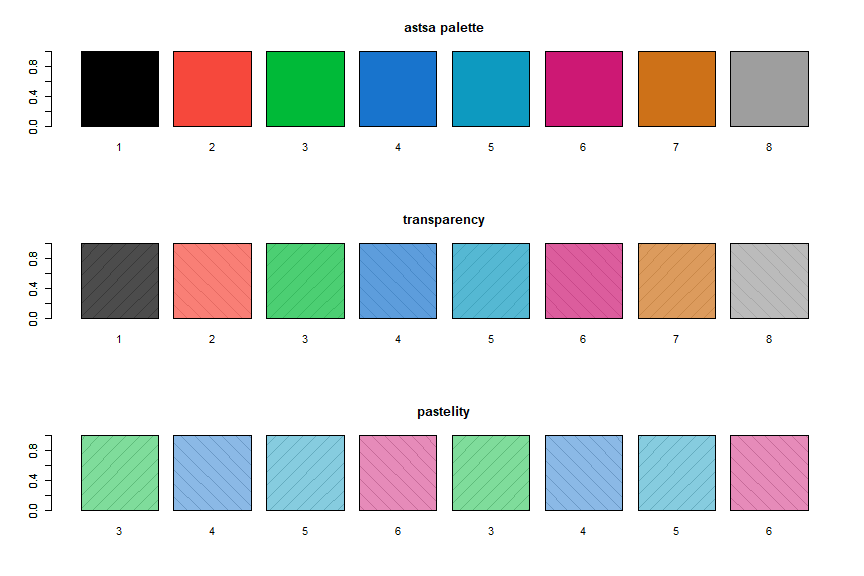

Colors

💡 When astsa is loaded, the astsa palette is attached. The palette is especially suited for plotting time series and it is a bit darker than the new default R4 palette. You can revert back using palette("default"). Also,

astsa.col()

is included to easily adjust the opacity of the colors.

par(mfrow=c(3,1))

barplot(rep(1,8), density=10, angle=c(45, -45), main='astsa palette')

barplot(rep(1,8), col=1:8, names=1:8, add=TRUE)

barplot(rep(1,8), density=10, angle=c(45, -45), main='transparency')

barplot(rep(1,8), col=astsa.col(1:8, .7), names=1:8, add=TRUE)

barplot(rep(1,8), density=10, angle=c(45, -45), main='pastelity')

barplot(rep(1,8), col=astsa.col(3:6, .5), names=rep(3:6, 2), add=TRUE)

Notice each color display has diagonal lines behind it to demonstrate opacity.

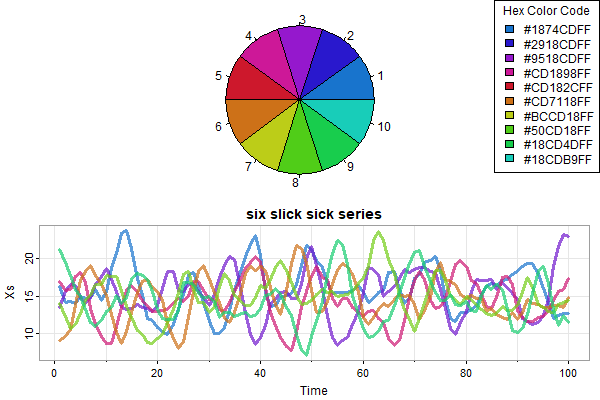

Color Wheel

🌈 NEW 🌈: astsa.col now can create a color wheel with a user specified number of colors based on a chosen color. Also included is the option to show a pie chart of the colors for inspection before use. Here’s some examples (with bells and whistles):

par(mfrow=2:1, mar=rep(0,4))

astsa.col(4, wheel=TRUE, pie=TRUE, num=10) -> u

legend('topright', legend=u, fill=u, title='Hex Color Code')

x = replicate(6, 15+sarima.sim(ar=c(1.5,-.75), n=100))

tsplot(x, ylab='Xs', main='six slick sick series', spag=TRUE, col=astsa.col(4, alpha=.7, wheel=TRUE, num=6), lwd=3)

tsplot

🔵 For plotting time series and just about anything else, you can use

tsplot()

👀 Notice there are minor ticks and a grid by default. Here are some examples.

par(mfrow=c(2,1))

tsplot(soi, col=4, lwd=2)

tsplot(soi, col=4, lwd=2, gg=TRUE) # gg => gris-gris plot - the grammar of astsa is voodoo

🔵 Many in one swell foop:

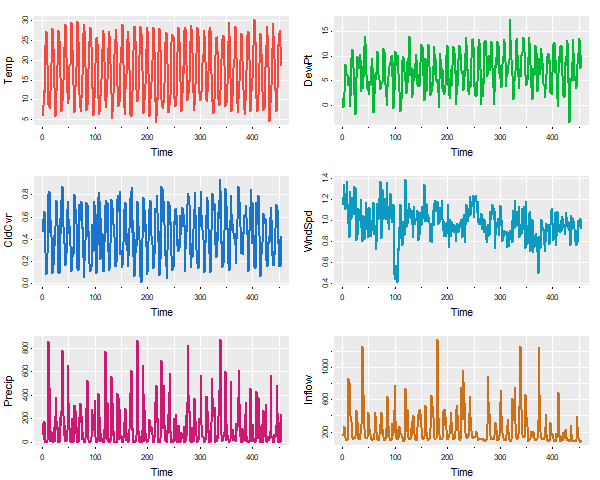

tsplot(climhyd, ncol=2, gg=TRUE, col=2:7, lwd=2)

The number of columns (ncolm) is user specified and not automated in any way.

🔵 Do you like spaghetti (you can shorten it to spag):

✔ In version 2.2 and beyond, you can use addLegend in tsplot with spaghetti plots (more than 1 series on the same plate).

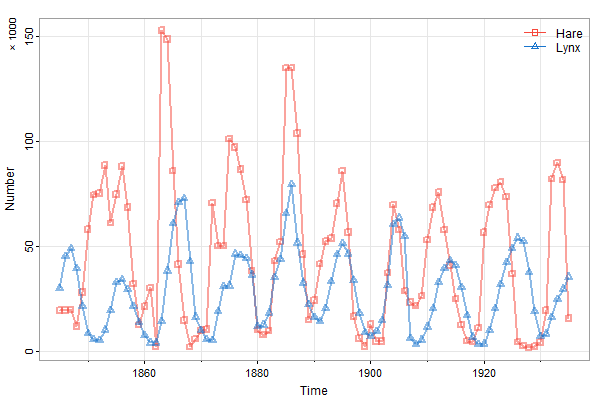

tsplot(cbind(Hare,Lynx), col=astsa.col(c(2,4),.5), lwd=2, type="o", pch=c(0,2),ylab='Number', spaghetti=TRUE, addLegend=TRUE)

mtext('\u00D7 1000', side=2, adj=1, line=1.5, cex=.8)

If you need more control, you can still use legend:

tsplot(cbind(Hare,Lynx), col=astsa.col(c(2,4),.5), lwd=2, type="o", pch=c(0,2), ylab='Number', spaghetti=TRUE)

mtext('\u00D7 1000', side=2, adj=1, line=1.5, cex=.8)

legend("topright", legend=c("Hare","Lynx"), col=c(2,4), lty=1, pch=c(0,2), bty="n")

🆒 And another easy-add legend for spaghetti plots:

# quick and easy legend

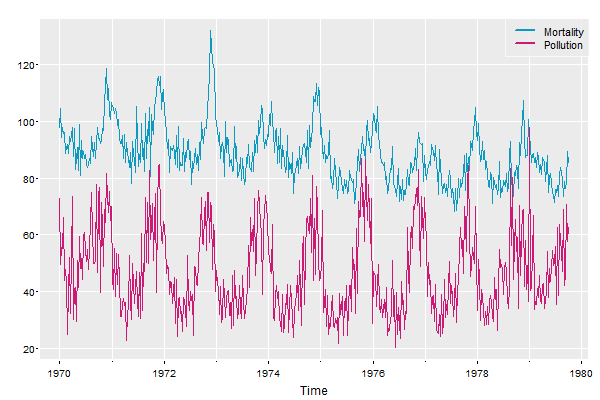

tsplot(cbind(Mortality=cmort, Pollution=part), col=5:6, gg=TRUE, spaghetti=TRUE, addLegend=TRUE, llwd=2)

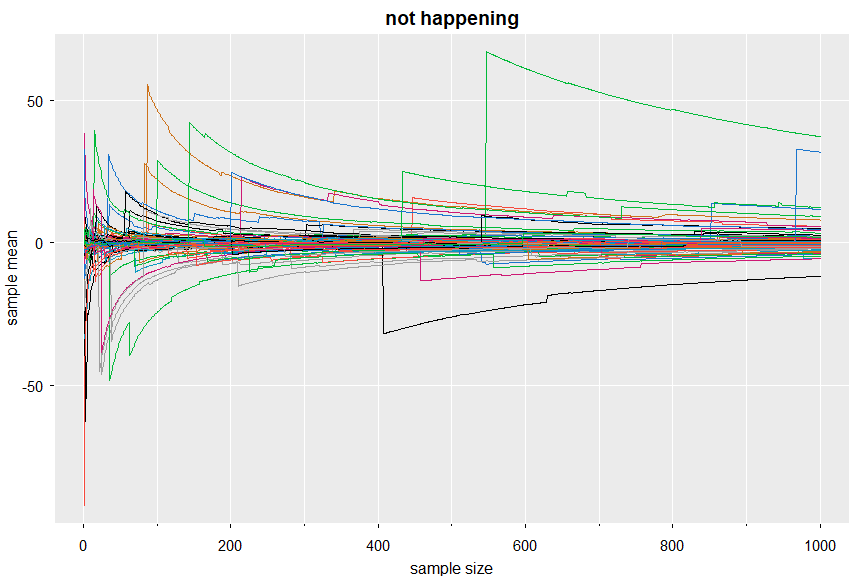

💔 And you can still have spaghetti in the land where the LLN ceases to exist:

x <- replicate(100, cumsum(rcauchy(1000))/1:1000)

tsplot(x, col=1:8, main='not happening', spaghetti=TRUE, gg=TRUE, ylab="sample mean", xlab="sample size")

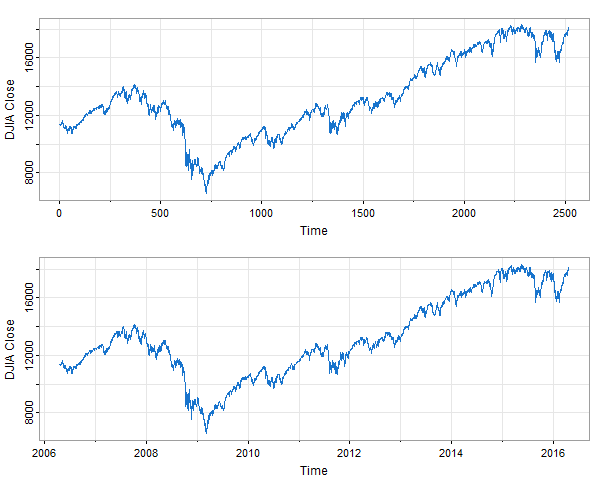

🆕 timex … keeps on ticking

There are a few xts data files in astsa and we recommend installing the package (and consequently zoo) if you are analyzing time series. But, in case xts is not available, you can still plot the series using the actual times as of astsa version 2.4.

Here’s an example using djia.

par(mfrow=2:1)

tsplot(djia[,'Close'], col=4, ylab='DJIA Close') # no dates

tsplot(timex(djia), djia[,'Close'], col=4, ylab='DJIA Close') # yes dates

In the top plot, the dates on the time axis are missing. The script timex takes the ‘unix time stamp’ dates from the xts data file and converts them to decimal time; e.g., September 1, 2010 is approximately 2010.666 because it is day 243 of that 365-day year (Jan 1 being day zero).

Lag Plots

🦄 There are also lag plots for one series and for two series using

lag1.plot()orlag2.plot()

By default, the graphic displays the sample ACF or CCF and a lowess fit. They can be turned off individually (?lag1.plot or ?lag2.plot for more info).

First, for one series

# minimal call

lag1.plot(soi, 12)

# but prettified

lag1.plot(soi, 12, col=astsa.col(4, .3), pch=20, cex=2)

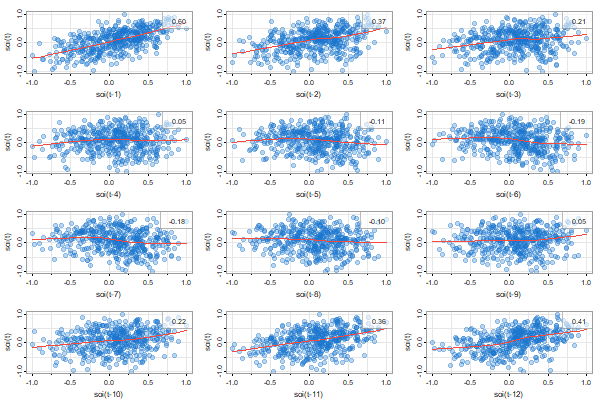

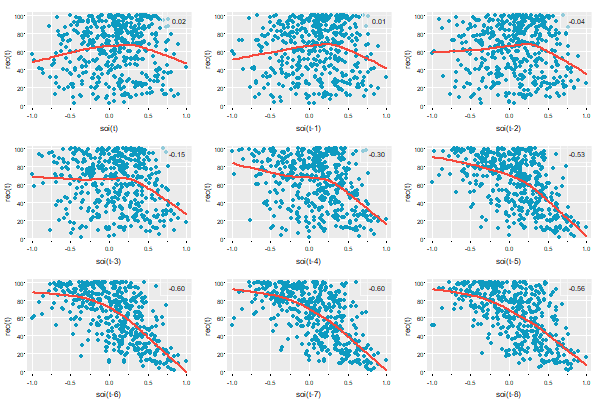

and for two series (the first one gets lagged)

# minimal call - the first series gets lagged

lag2.plot(soi, rec, 8)

# but prettified

lag2.plot(soi, rec, 8, pch=19, col=5, lwl=2, gg=TRUE)

As of version 2.3, you can change the location of the ACF values:

lag2.plot(soi, rec, 8, pch=19, col=astsa.col(4,.3), gg=TRUE, location='bottomleft')

🐭 As previously mentioned, you can turn off the correlation or smooth displays by setting those things to FALSE (in either script); e.g.,

lag1.plot(diff(log(GDP)), 4, corr=FALSE, smooth=FALSE) # not shown

Scatterplots

Aside from lag plots, we have some additional scripts for doing scatterplot matrices.

🐹 There is now tspairs, which is an astsa version of stats::pairs for time series. It’s used in ar.boot and ar.mcmc now. Here are two examples:

tspairs(diff(log(econ5[,1:3])), col.diag=6, pt.size=1.5, lwl=2, gg=TRUE, las=0)

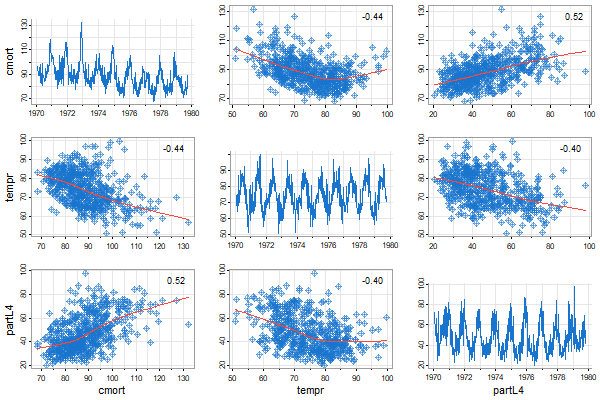

tspairs(ts.intersect(cmort,tempr,partL4=lag(part,-4)), hist=FALSE, pch=9, scale=1.1)

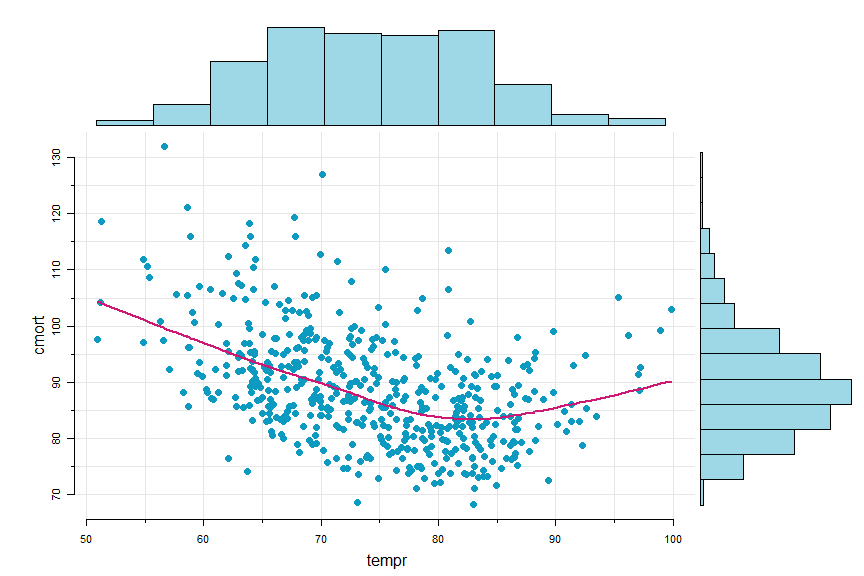

🐛 Sometimes it’s nice to have a scatterplot with marginal histograms…

scatter.hist(tempr, cmort, hist.col=astsa.col(5,.4), pt.col=5, pt.size=1.5, reset=FALSE)

lines(lowess(tempr, cmort), col=6, lwd=2) # with reset=FALSE, can add to the scatterplot

Trends

💲 There are two scripts to help with analyzing trends. They are

detrend()andtrend()

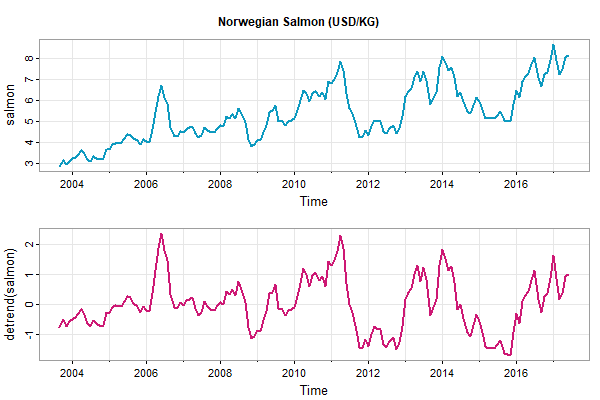

🔵 detrend returns a detrended series using a polynomial regression (default is linear) or lowess (with the default span). For example,

tsplot(cbind(salmon, detrend(salmon)), main='Norwegian Salmon (USD/KG)', lwd=2, col=5:6)

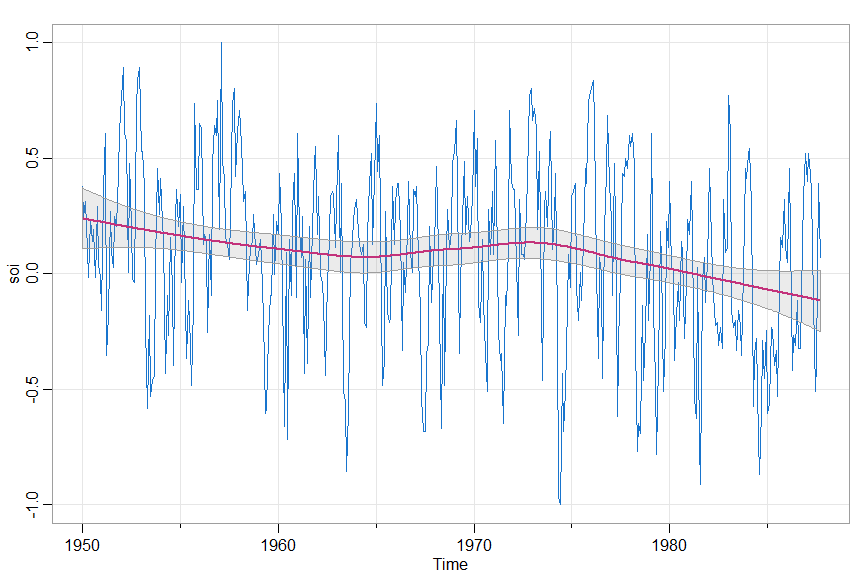

🐽 trend fits a trend (same options as detrend) and produces a graphic of the series with the trend and error bounds superimposed. The trend and error bounds are returned invisibly.

trend(soi, lowess=TRUE)

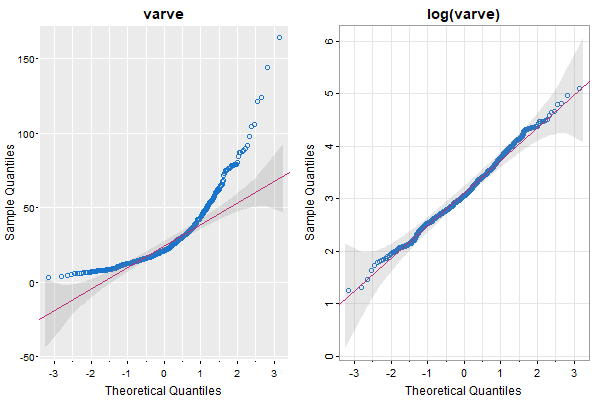

QQnorm

🦄 The texts have a few QQ plots and we needed them to look good because the importance of appearance extends well beyond the pleasant experiences we have when we look at attractive plots. And the code was sitting there in sarima as part of the diagnostics, so we just pulled it out.

par(mfrow=1:2)

QQnorm(varve, main='varve', gg=TRUE)

QQnorm(log(varve), main='log(varve)')

Regression t-table with VIFs

🐭 It’s not a graphic thing, but there was no other place to put this with ease. This is used in the 2nd edition of the Chapman Hall text. It is available in astsa version 2.3 and beyond. It’s based on summary.lm but it prints AIC, AICc, and BIC and it can include VIFs if appropriate and it goes like this:

fit = lm( mpg~ cyl + disp + hp + drat + wt + qsec, data=mtcars)

ttable(fit, vif=TRUE)

## output

Coefficients:

Estimate SE t.value p.value VIF

(Intercept) 26.3074 14.6299 1.7982 0.0842

cyl -0.8186 0.8116 -1.0086 0.3228 9.9590

disp 0.0132 0.0120 1.0971 0.2831 10.5506 <- engine size

hp -0.0179 0.0155 -1.1564 0.2585 5.3578

drat 1.3204 1.4795 0.8925 0.3806 2.9665

wt -4.1908 1.2579 -3.3316 0.0027 7.1817

qsec 0.4015 0.5166 0.7771 0.4444 4.0397

Residual standard error: 2.557 on 25 degrees of freedom

Multiple R-squared: 0.8548, Adjusted R-squared: 0.82

F-statistic: 24.53 on 6 and 25 DF, p-value: 2.45e-09

AIC = 3.1309 AICc = 3.2768 BIC = 3.4974

mtcars is an R data set on gas consumption (mpg) and various car design aspects (the ‘mt’ refers to ‘motor trend’ magazine). The design aspects are related [bigger engines have more horse power and weight …], thus the high VIFs. Also notice that the engine size (disp) coefficient has the wrong sign because bigger engines don’t get better gas mileage. Also, nothing but weight (wt) is significant because the SEs are inflated. How’s that for a picture?

😈 Well- since this is the part with a lot of pictures, and this regression example doesn’t come with any, we decided to put up this nice picture … enjoy:

3. Correlations

👽 There are four basic correlation scripts and one not so basic script in astsa. They are

acf1(),acf2(),ccf2(),acfm(), andpre.white()

-

acf1gives the sample ACF or PACF of a series. -

acf2gives both the sample ACF and PACF in a multifigure plot and both on the same scale. The graphics do not display the lag 0 ACF value because it is always 1. -

ccf2plots the sample CCFacf1andacf2also print the values, but rounded -ccf2returns the values invisibly -

acfmis for multiple time series and it produces a grid of plots of the sample ACFs and CCFs. -

pre.white(in version 2.2) will prewhiten the first series automatically, filter the second accordingly, and perform a cross-correlation analysis.

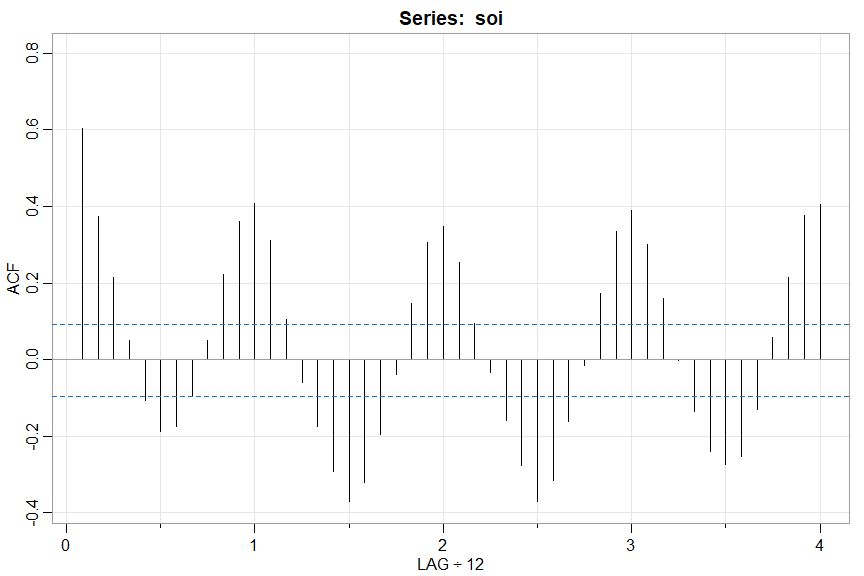

🔵 The individual sample ACF or PACF

acf1(soi)

[1] 0.60 0.37 0.21 0.05 -0.11 -0.19 -0.18 -0.10 ...

💡 Note the LAG axis label indicates the frequency of the data unless it is 1. This way, you can see that the tick at LAG 1 corresponds to 12 (months) and so on.

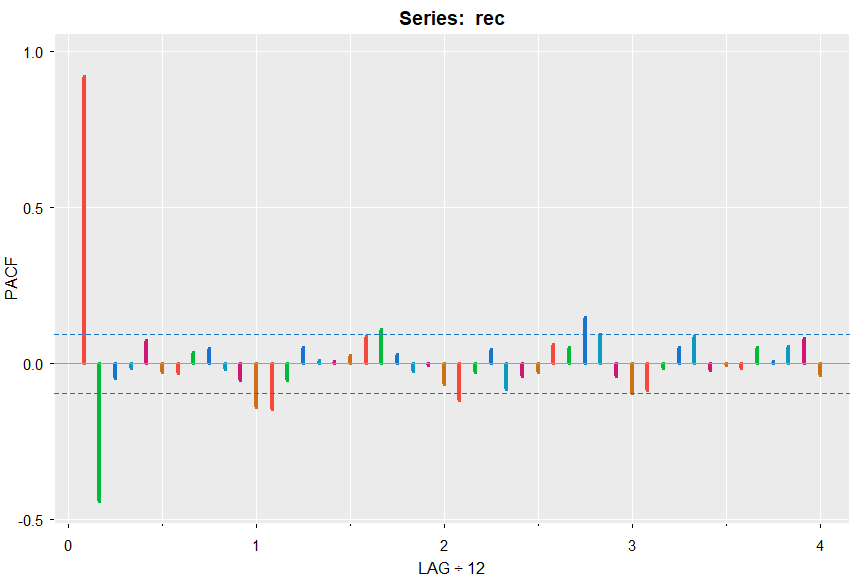

acf1(rec, pacf=TRUE, gg=TRUE, col=2:7, lwd=4)

[1] 0.92 -0.44 -0.05 -0.02 0.07 -0.03 -0.03 0.04 ...

🔵 Sample ACF and PACF at the same time

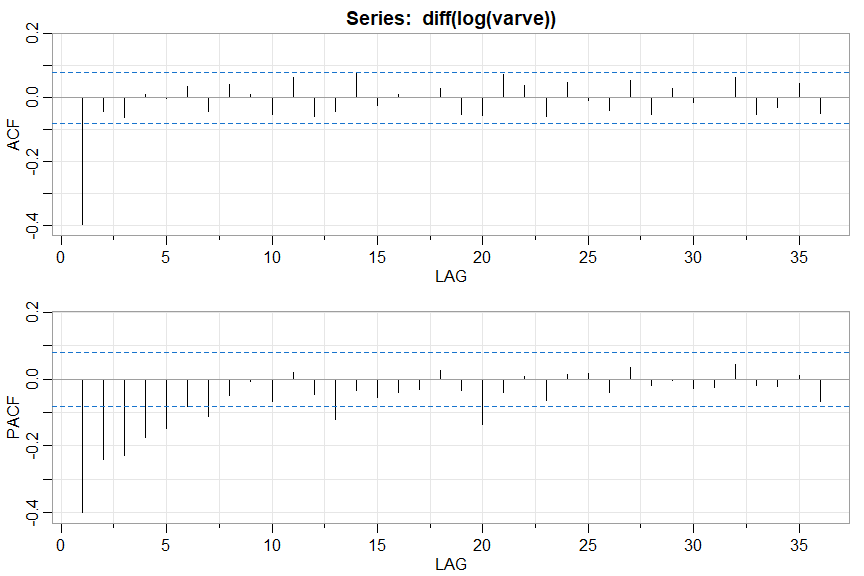

acf2(diff(log(varve)))

[,1] [,2] [,3] [,4] [,5] [,6] [,7] [,8] [,9] ...

ACF -0.4 -0.04 -0.06 0.01 0.00 0.04 -0.04 0.04 0.01 ...

PACF -0.4 -0.24 -0.23 -0.18 -0.15 -0.08 -0.11 -0.05 -0.01 ...

🔵 If you just want the values (not rounded by the script), use plot=FALSE (works for acf1 too)

acf2(diff(log(varve)), plot=FALSE)

ACF PACF

[1,] -0.3974306333 -0.397430633

[2,] -0.0444811551 -0.240404406

[3,] -0.0637310878 -0.228393075

[4,] 0.0092043800 -0.175778181

[5,] -0.0029272130 -0.148565114

[6,] 0.0353209520 -0.080800502

. . .

[33,] -0.0516758878 -0.017946464

[34,] -0.0308370865 -0.021854959

[35,] 0.0431050489 0.010867281

[36,] -0.0503025493 -0.068574763

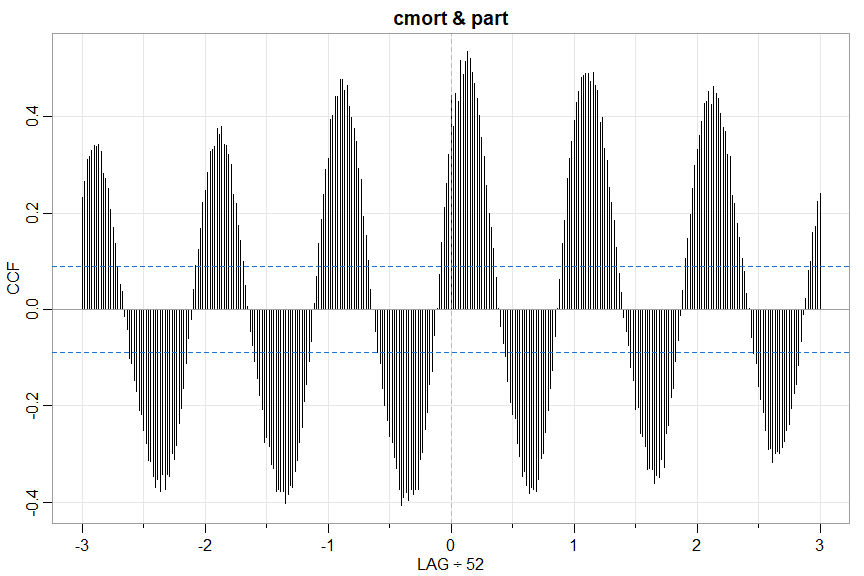

🔵 and the sample CCF

ccf2(cmort, part)

🚫 Don’t be fooled because neither series is white noise - far from it. Prewhiten before a real cross-correlation analysis (but you know that already because you’ve read it in one of the books).

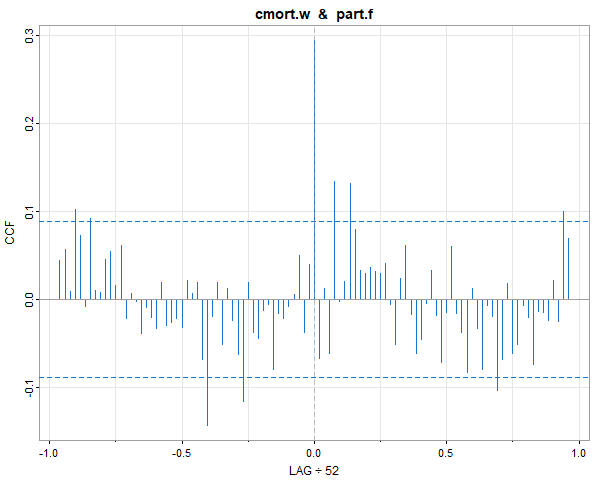

🤑 Here’s a way to do it using pre.white from astsa version 2.2 (it’s semiautomatic- the user has to decide if differencing is necessary):

pre.white(cmort, part, diff=TRUE, col=4) # in version 2.2

# with output

cmort prewhitened using an AR p = 3

after differencing d = 1

# and ...

… you get a graphic. The transformed series are returned invisibly (the .w is for whitened and the .f is for filtered):

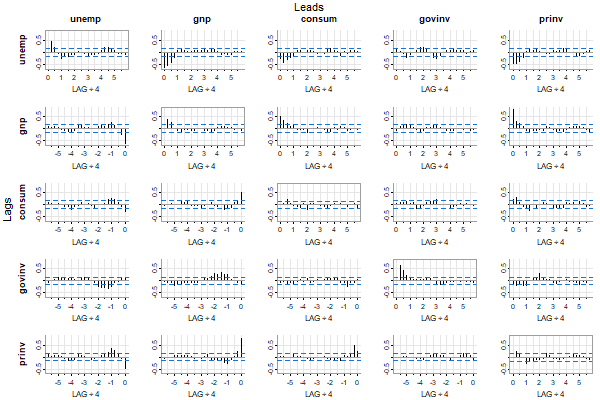

🔵 For multiple series, you can look at all sample ACFs (highlighted a bit on the diagonal) and CCFs (off-diagonal) simultaneously:

acfm(diff(log(econ5)))

What you see are estimates of corr( xt+LAG , yt ) where xt is a column series and yt is a row series. xt leads when LAG is positive and xt lags when LAG is negative. In the figure, the top (columns) series leads and the side series (rows) lags.

All of these scripts use tsplot so there are various options for plotting. For example, you can suppress the minor ticks if it’s too much, or you can do a “gris-gris” plot (the grammar of astsa is voodoo):

acfm(diff(log(econ5)), nxm=0) # no minor ticks on LAG axis

acfm(diff(log(econ5)), gg=TRUE, acf.highlight=FALSE) # Gris-Gris Gumbo Ya Ya

4. ARIMA

ARMA Model Evaluation

🤪 Checking the validity of an ARMA model (seasonal ok) just got easier with arma.check. Let’s look at some examples with output.

arma.check(ar=.9, ma=-.88)

# WARNING: (Possible) Parameter Redundancy

#

# It looks like that ARMA model has (approximate) common factors.

# This means that the model is (possibly) over-parameterized.

# You might want to try again.

arma.check(ar=c(1,-.9), sar=-.6, sma=-.4, S=4)

# The model is causal.

# The model is invertible.

# That's a very nice ARMA model!

arma.check(ma=1, sar=1, S=12)

# WARNING: Model Not Invertible

# WARNING: Seasonal Part Not Causal

# NOTE: Redundancy checked only for causal and invertible models

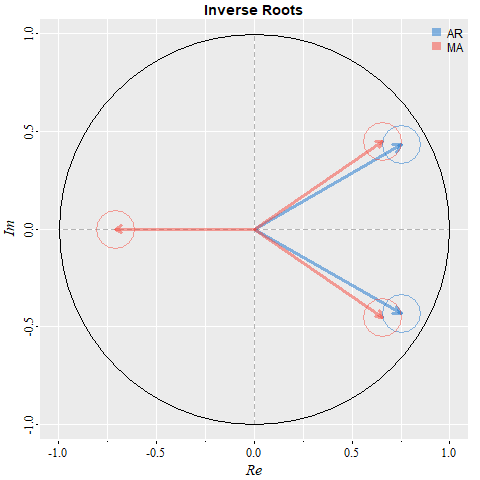

You want a picture? Ok, but any seasonal stuff is ignored to avoid a messy graphic. It’s the complex plane with the inverse roots and the little circles have the radius of the redundancy tolerance, which may be set by the user (?arma.check has details). Also, the graphic is displayed ONLY for causal and invertible models (so all inverted roots are within the unit circle).

arma.check(ar=c(1.5,-.75), ma=c(-.6,-.3,.45), plot=TRUE, gg=TRUE)

# WARNING: (Possible) Parameter Redundancy ...

##- this is not output... but just a little note that you can't

##- always tell if a model is overparameterized just by looking

##- at the parameters (unless you have extraordinary skills)

ARIMA Simulation

💫 You can simulate from ARIMA models - seasonal or non-seasonal - via

sarima.sim()

The syntax are simple and we’ll demonstrate with a couple of examples. There are more examples in the help file (?sarima.sim). For example, you can input your own innovations or generate non-normal innovations (the default is normal).

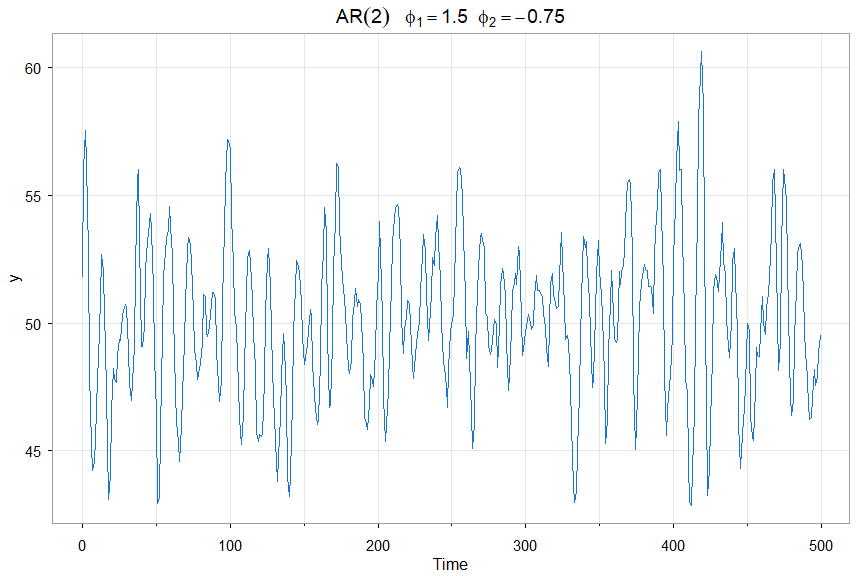

🔵 First an AR(2) with a mean of 50 (n=500 is the default sample size)

y = sarima.sim(ar=c(1.5,-.75)) + 50

tsplot(y, main=bquote(AR(2)~~~phi[1]==1.5~~phi[2]==-.75), col=4)

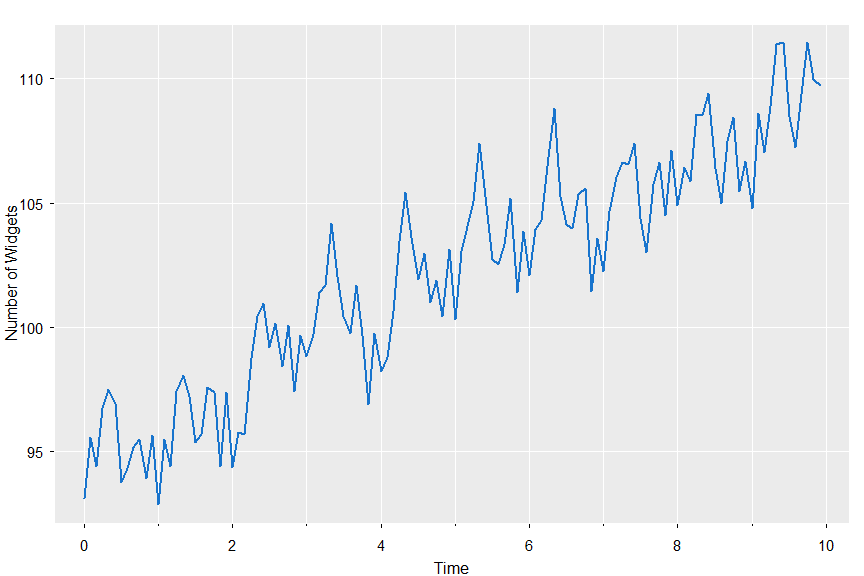

🔵 Now we’ll simulate from a seasonal model, SARIMA(0,1,1)x(0,1,1)12 — B&J’s favorite

set.seed(101010)

x = sarima.sim(d=1, ma=-.4, D=1, sma=-.6, S=12, n=120) + 100

tsplot(x, col=4, lwd=2, gg=TRUE, ylab='Number of Widgets')

ARIMA Estimation

🍉 Fitting ARIMA models to data is a breeze with the script

sarima()

It can do everything for you but you have to choose the model … speaking of which …

❌ Don’t use black boxes like auto.arima from the forecast package because IT DOESN’T WORK well. If you know what you are doing, fitting an ARIMA model to linear time series data is easy.

Originally, astsa had a version of automatic fitting of models but IT DIDN’T WORK and was scrapped. The bottom line is, if you don’t know what you’re doing (aka ZERO KNOWLEDGE), why are you doing it? Maybe a better idea is to take a short course on fitting ARIMA models to data.

DON’T BELIEVE IT?? OK… HERE YOU GO:

set.seed(666)

x = rnorm(1000) # WHITE NOISE

forecast::auto.arima(x) # BLACK BOX

# partial output

Series: x

ARIMA(2,0,1) with zero mean

Coefficients:

ar1 ar2 ma1

-0.9744 -0.0477 0.9509

s.e. 0.0429 0.0321 0.0294

sigma^2 estimated as 0.9657: log likelihood=-1400

AIC=2808.01 AICc=2808.05 BIC=2827.64

🤣🤣🤣 … an ARMA(2,1) ?? BUT, if you KNOW what you are doing, you realize the model is basically overparametrized white noise … CHECK IT OUT:

arma.check(ar=c(-.9744, -.0477), ma=.9509)

WARNING: (Possible) Parameter Redundancy

It looks like that ARMA model has (approximate) common factors.

This means that the model is (possibly) over-parameterized.

You might want to try again.

Here’s another humorous example. Using the data cmort (cardiovascular mortality)

forecast::auto.arima(cmort)

Series: cmort

ARIMA(2,0,2)(0,1,0)[52] with drift

Coefficients:

ar1 ar2 ma1 ma2 drift

0.5826 0.0246 -0.3857 0.2479 -0.0203

s.e. 0.3623 0.3116 0.3606 0.2179 0.0148

sigma^2 = 56.94: log likelihood = -1566.28

AIC=3144.57 AICc=3144.76 BIC=3169.3

HA! Five parameters and none significant in a rather complex seasonal model. AND, it took forever to run during which my CPU fan speed ran on high. By overfitting, the standard errors are inflated.

But, if you know what you’re doing, difference to remove the trend, then it’s obviously an AR(1):

sarima(cmort, 1,1,0, no.constant=TRUE)

Coefficients:

Estimate SE t.value p.value

ar1 -0.5064 0.0383 -13.2224 0

sigma^2 estimated as 33.81057 on 506 degrees of freedom

AIC = 6.367124 AICc = 6.36714 BIC = 6.383805

Yep!! 1 parameter with a decent standard error and the residuals are perfect (white and normal).

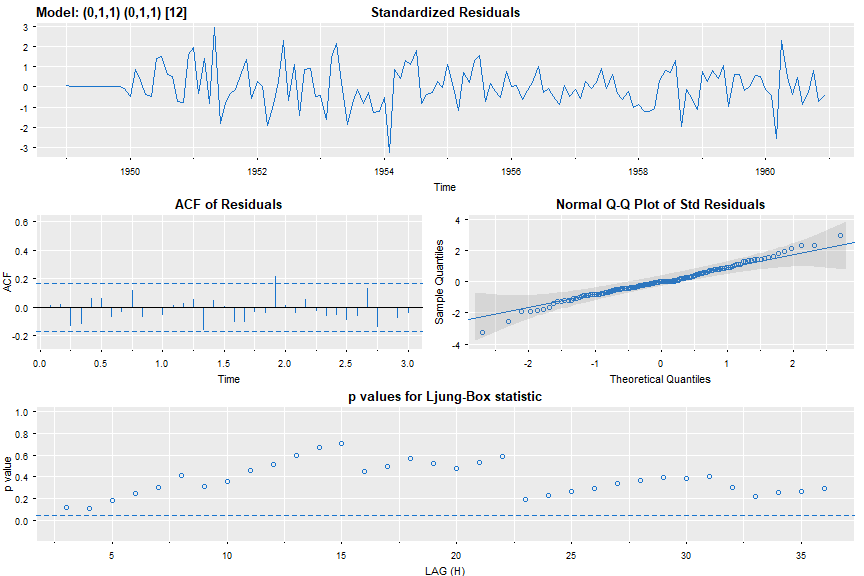

👽 Ok - back to our regularly scheduled program, sarima(). As with everything else, there are many examples on the help page (?sarima) and we’ll do a couple here.

🔵 Everyone else does it, so why don’t we. Here’s a seasonal ARIMA fit to the AirPassenger data set (for the millionth time).

sarima(log(AirPassengers),0,1,1,0,1,1,12, gg=TRUE, col=4)

and the partial output including the residual diagnostic plot is (AIC is basically aic divided by the sample size):

Coefficients:

Estimate SE t.value p.value

ma1 -0.4018 0.0896 -4.4825 0

sma1 -0.5569 0.0731 -7.6190 0

sigma^2 estimated as 0.001348035 on 129 degrees of freedom

AIC = -3.690069 AICc = -3.689354 BIC = -3.624225

🔵 You can shut off the diagnostics using details=FALSE

sarima(log(AirPassengers),0,1,1,0,1,1,12, details=FALSE)

🔵 You can fix parameters too, for example

x = sarima.sim( ar=c(0,-.9), n=200 ) + 50

sarima(x, 2,0,0, fixed=c(0,NA,NA)) # ar1 (fixed at 0), ar2 (NA -> free), mean (NA -> free)

with output

Coefficients:

Estimate SE t.value p.value

ar2 -0.9319 0.0246 -37.9526 0

xmean 49.9527 0.0367 1361.7834 0

sigma^2 estimated as 0.9946776 on 198 degrees of freedom

AIC = 2.882823 AICc = 2.883128 BIC = 2.932298

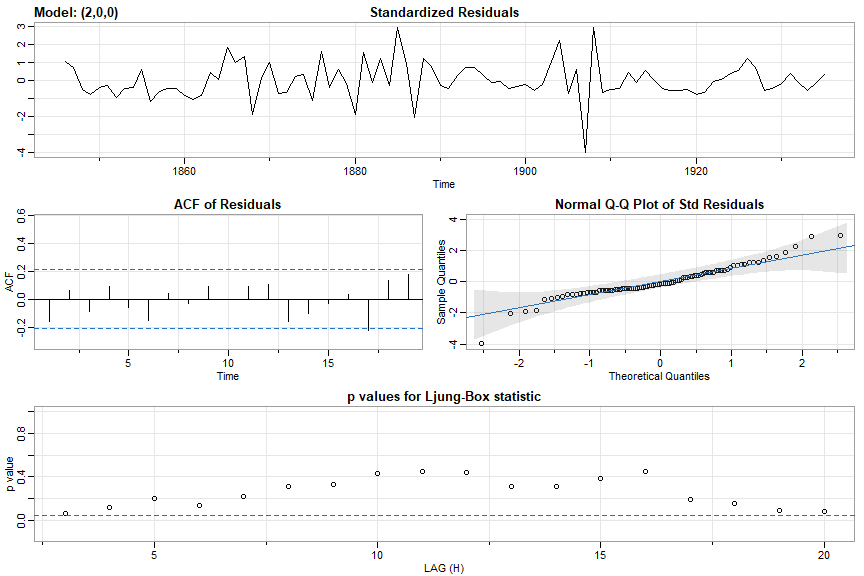

🔵 And one more with exogenous variables - this is the regression of Lynx on Hare lagged one year with AR(2) errors.

pp = ts.intersect(Lynx, HareL1 = lag(Hare,-1), dframe=TRUE)

sarima(pp$Lynx, 2,0,0, xreg=pp$HareL1)

with partial output

Coefficients:

Estimate SE t.value p.value

ar1 1.3258 0.0732 18.1184 0.0000

ar2 -0.7143 0.0731 -9.7689 0.0000

intercept 25.1319 2.5469 9.8676 0.0000

xreg 0.0692 0.0318 2.1727 0.0326

sigma^2 estimated as 59.57091 on 86 degrees of freedom

AIC = 7.062148 AICc = 7.067377 BIC = 7.201026

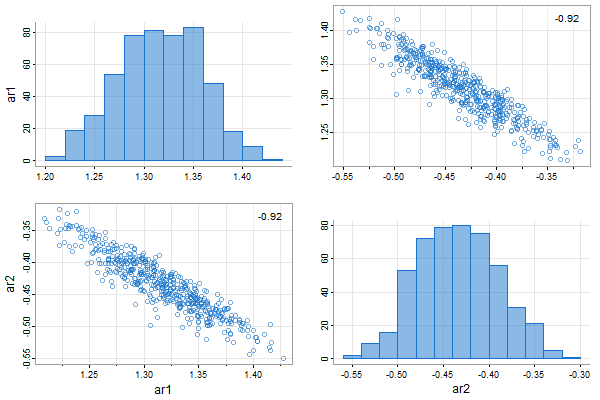

👾 And you can fit AR models using the bootstrap. Let’s fit an AR(2) to the Recruitment series.

ar.boot(rec, 2)

## output: ##

Quantiles:

ar1 ar2

1% 1.205 -0.5338

2.5% 1.234 -0.5186

5% 1.249 -0.5021

10% 1.266 -0.4912

25% 1.294 -0.4656

50% 1.326 -0.4429

75% 1.354 -0.4121

90% 1.376 -0.3874

95% 1.393 -0.3682

97.5% 1.406 -0.3589

99% 1.413 -0.3443

Mean:

ar1 ar2

1.3229 -0.4404

Bias:

ar1 ar2

[1,] -0.008703 0.004168

rMSE:

ar1 ar2

[1,] 0.04479 0.04192

and a picture (uses tspairs for output):

Forecasting

🌹 Forecasting your fitted ARIMA model is as simple as using

sarima.for()

You get a graphic showing ± 1 and 2 root mean square prediction errors and the predictions and standard errors are printed. The syntax are similar to sarima but the number of periods to forecast, n.ahead, has to be specified.

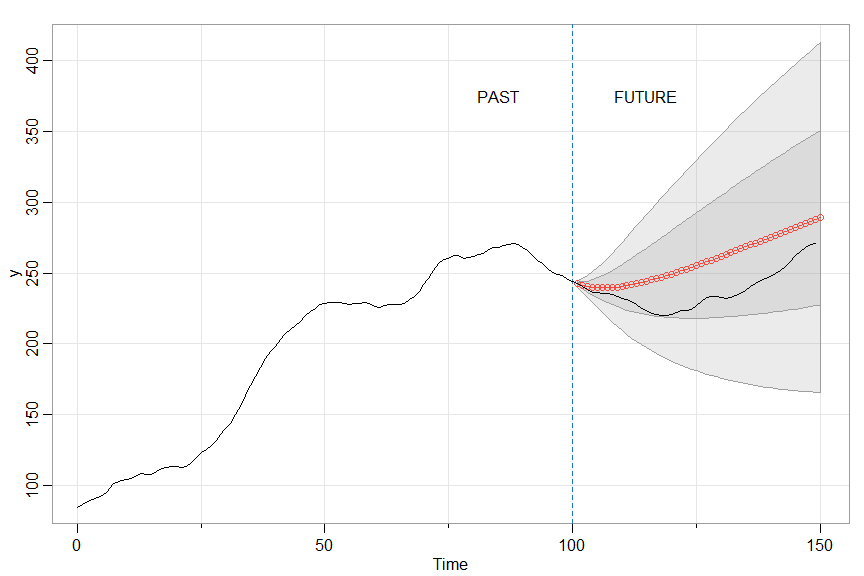

🔵 Here’s a simple example. We’ll generate some data from an ARIMA(1,1,0), forecast some of it and then compare the forecasts to the actual values.

set.seed(12345)

x <- sarima.sim(ar=.9, d=1, n=150) # 150 observations

y <- window(x, start=1, end=100) # use first 100 to forecast

sarima.for(y, n.ahead=50, p=1, d=1, q=0, plot.all=TRUE)

text(85, 375, "PAST"); text(115, 375, "FUTURE")

abline(v=100, lty=2, col=4)

lines(x)

with partial output

$pred

Time Series:

Start = 101

End = 150

Frequency = 1

[1] 242.3821 241.3023 240.5037 239.9545 239.6264 239.4945 239.5364 ...

$se

Time Series:

Start = 101

End = 150

Frequency = 1

[1] 1.136849 2.427539 3.889295 5.459392 7.096606 8.772528 10.466926 ...

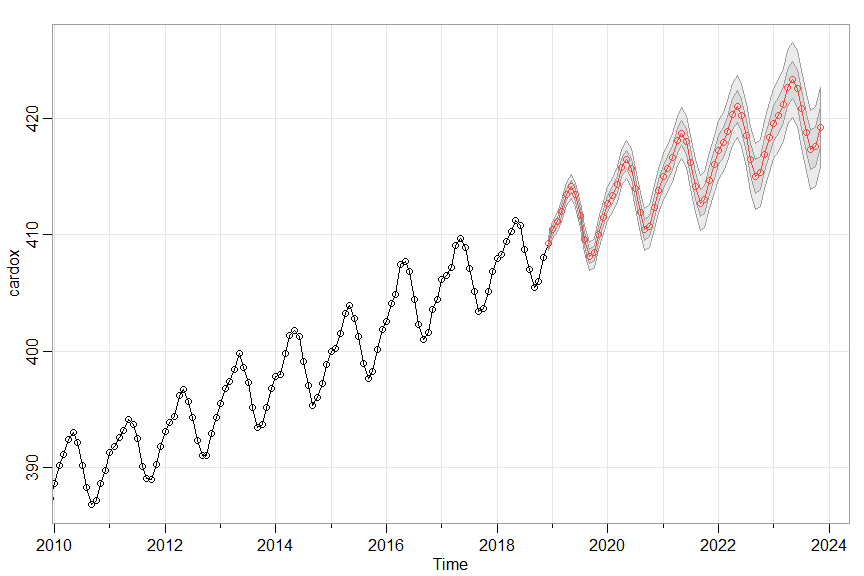

🔵 Notice the plot.all=TRUE in the sarima.for call. The default is FALSE in which case the graphic shows only the final 100 observations and the forecasts to make it easier to see what’s going on (like in the next example).

sarima.for(cardox, 60, 1,1,1, 0,1,1,12)

Missing Data

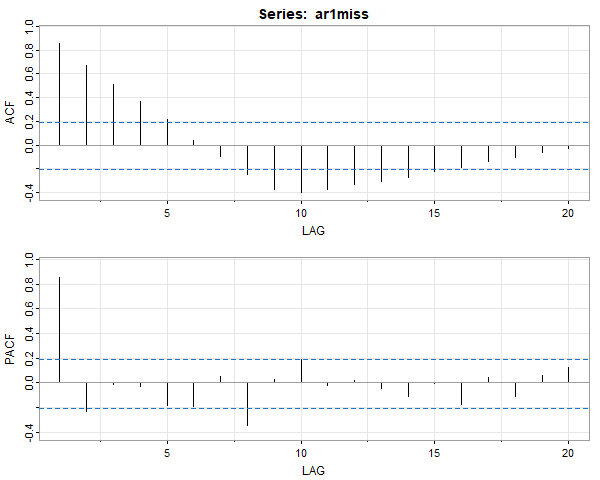

Because ARIMA models are put into state space form for estimation, missing data can be handled easily. There is a data file in astsa called ar1miss that has missing data (it’s used in Chapter 6 Problems – you’ll see the data in the forecast plot):

# as long as there aren't too many NAs, you can

# use acf2() to check an AR(1) is appropriate

acf2(ar1miss, na.action=na.contiguous)

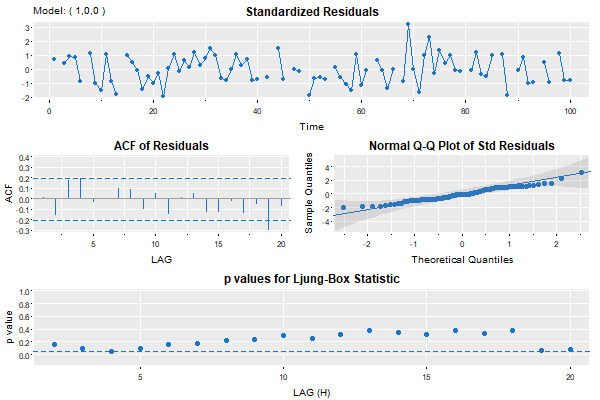

sarima(ar1miss, p=1, col=4, pch=19, gg=TRUE)

###- some output -###

# iter 2 value 0.174072

# . . .

# iter 10 value 0.136904

# converged

# <><><><><><><><><><><><><><>

#

# Coefficients:

# Estimate SE t.value p.value

# ar1 0.7684 0.0641 11.9848 0.0000

# xmean -0.2259 0.4588 -0.4923 0.6238

# sigma^2 estimated as 1.198931 on 83 degrees of freedom

# AIC = 3.182273 AICc = 3.183995 BIC = 3.268484

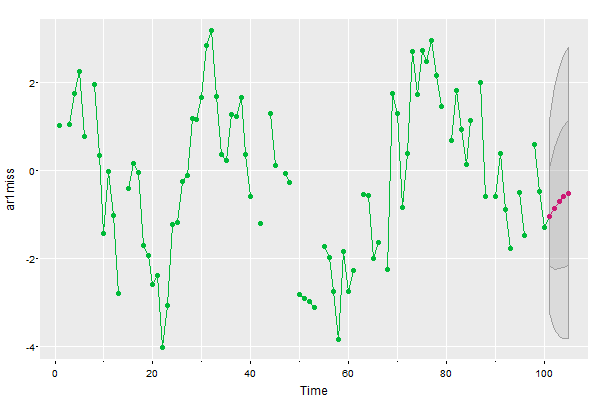

sarima.for(ar1miss, n.ahead=5, p=1, col=3, pcol=6, pch=19, gg=TRUE)

5. Spectral Analysis

🌞 There are a few scripts that help with spectral analysis.

The spectral density of an ARMA model can be obtained using

arma.spec()

Nonparametric spectral analysis is done with

mvspec()

and parametric spectral analysis with

spec.ic()

ARMA Spectral Density

💡 arma.spec tests for causality, invertibility, and common zeros. If the model is not causal or invertible an error message is given. If there are approximate common zeros, a spectrum will be displayed and a warning will be given. The frequency and spectral ordinates are returned invisibly.

arma.spec(ar = c(1.5, -.75), ma = c(-.8,.4), col=4, lwd=2)

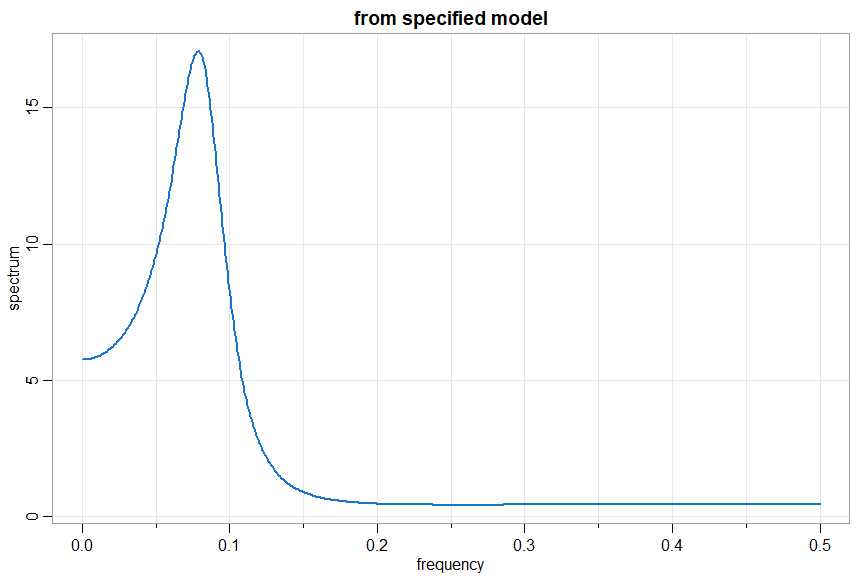

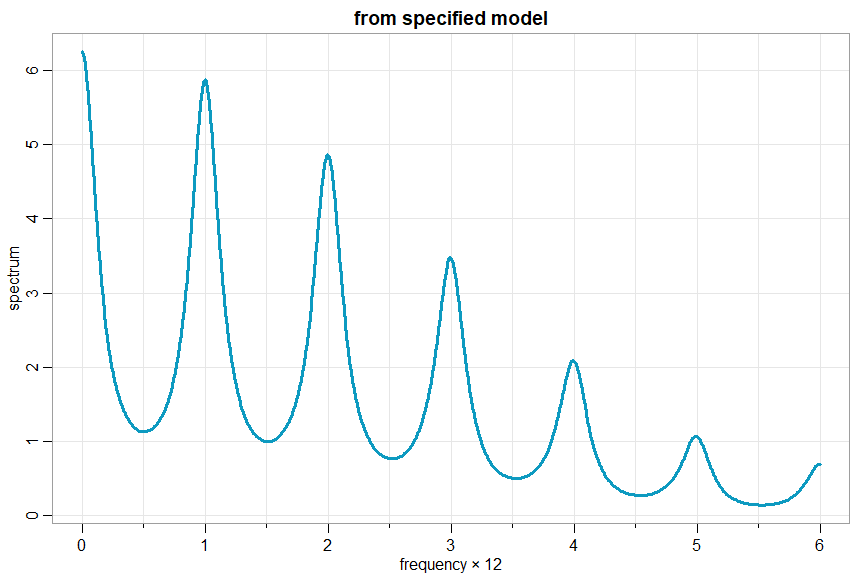

and if you want to do a seasonal model, you have to be a little creative; e.g., xt= .4 xt-12 + wt + .5 wt-1

arma.spec(ar=c(rep(0,11),.4), ma=.5, col=5, lwd=3, frequency=12)

Some goofs

arma.spec(ar=10, ma=20)

WARNING: Model Not Causal

WARNING: Model Not Invertible

Error in arma.spec(ar = 10, ma = 20) : Try Again

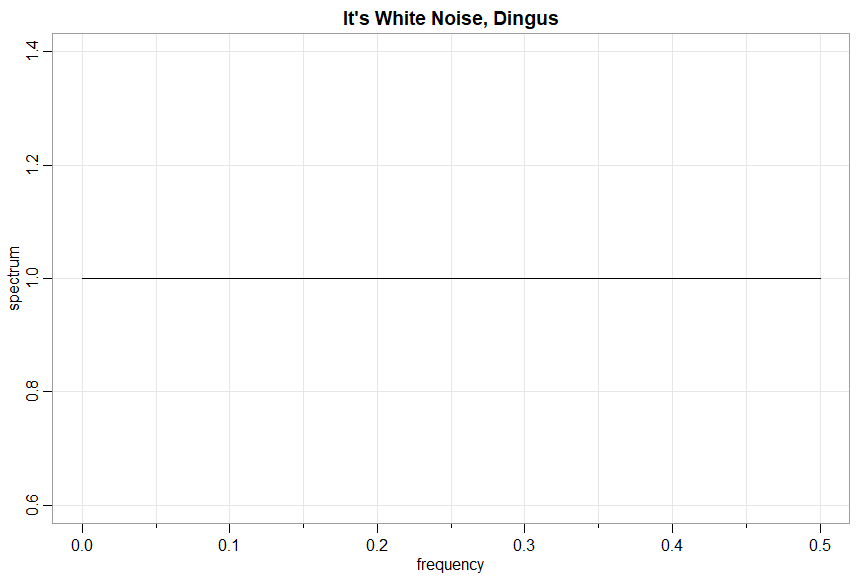

arma.spec(ar= .9, ma= -.9, main="It's White Noise, Dingus")

WARNING: Parameter Redundancy

nonparametric spectral analysis

🎹 mvspec was originally just a way to get the multivariate spectral density estimate out of spec.pgram directly (without additional calculations), but then it turned into its own pretty little monster with lots of bells and whistles.

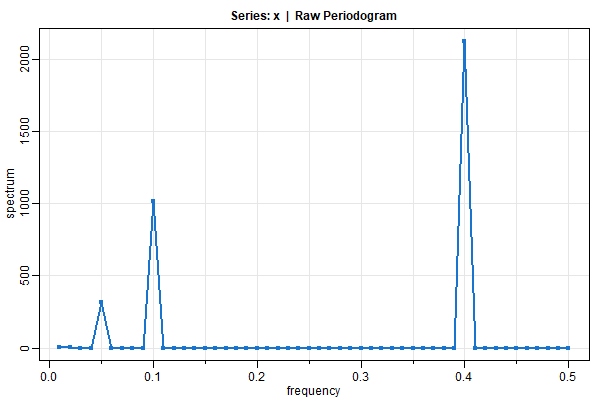

🔵 If you want the periodogram, you got it (tapering is not done automatically because you’re old enough to do it by yourself):

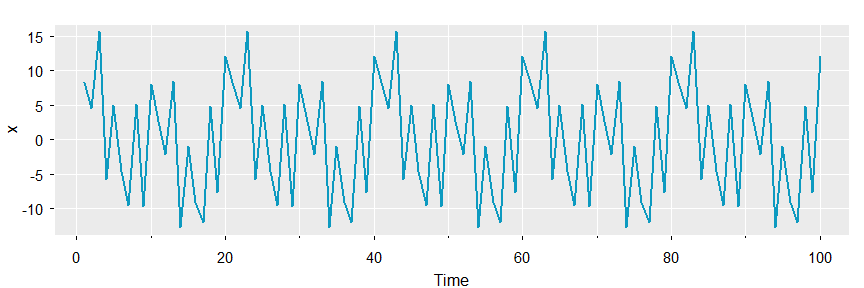

x1 = 2*cos(2*pi*1:100*5/100) + 3*sin(2*pi*1:100*5/100)

x2 = 4*cos(2*pi*1:100*10/100) + 5*sin(2*pi*1:100*10/100)

x3 = 6*cos(2*pi*1:100*40/100) + 7*sin(2*pi*1:100*40/100)

x = x1 + x2 + x3

tsplot(x, col=5, lwd=2, gg=TRUE)

mvspec(x, col=4, lwd=2, type='o', pch=20)

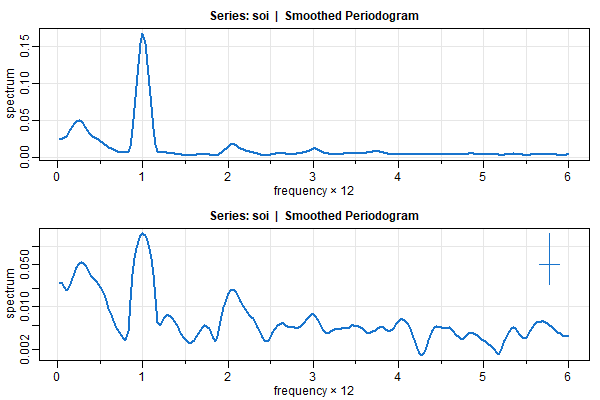

🔵 You can smooth in the usual way and get the CIs on the log-plot:

par(mfrow=c(2,1))

sois = mvspec(soi, spans=c(7,7), taper=.1, col=4, lwd=2)

##-- these get printed unless plot=FALSE--##

# Bandwidth: 0.231 | Degrees of Freedom: 8.96 | split taper: 10%

soisl = mvspec(soi, spans=c(7,7), taper=.5, col=4, lwd=2, log='y')

# ditto

🔵 and you can easily locate the peaks

sois$details[1:45,]

frequency period spectrum

[8,] 0.200 5.0000 0.0461

[9,] 0.225 4.4444 0.0489

[10,] 0.250 4.0000 0.0502 <- here

[11,] 0.275 3.6364 0.0490

[12,] 0.300 3.3333 0.0451

[13,] 0.325 3.0769 0.0403

[14,] 0.350 2.8571 0.0361

[38,] 0.950 1.0526 0.1253

[39,] 0.975 1.0256 0.1537

[40,] 1.000 1.0000 0.1675 <- here

[41,] 1.025 0.9756 0.1538

[42,] 1.050 0.9524 0.1259

[43,] 1.075 0.9302 0.0972

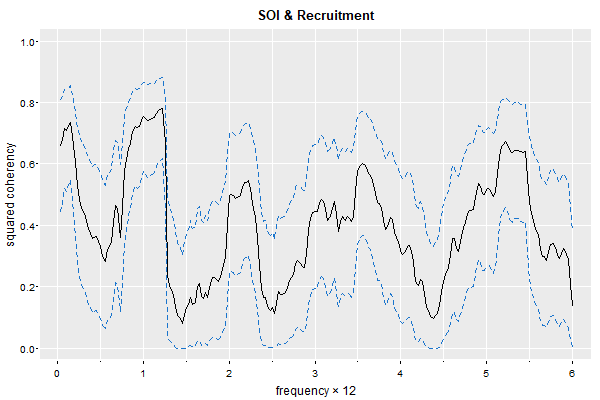

🔵 and cross-spectra

mvspec(cbind(soi,rec), spans=20, plot.type="coh", taper=.1, ci.lty=2, gg=TRUE, main="SOI & Recruitment")

# Bandwidth: 0.513 | Degrees of Freedom: 34.68 | split taper: 10%

parametric spectral analysis

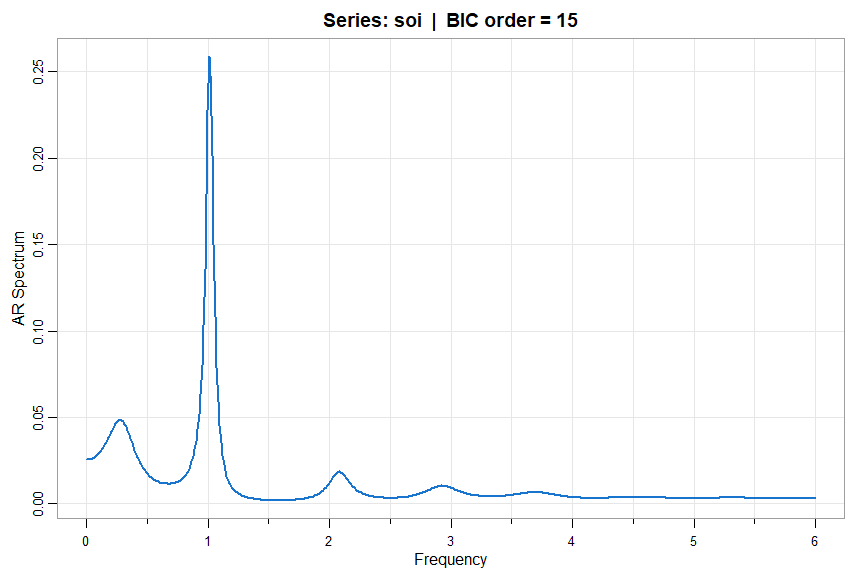

💡 spec.ic (in astsa) is similar to spec.ar (in stats) but the option to use BIC instead of AIC is available. Also, you can use the script to compare AIC and BIC for AR fits to the data.

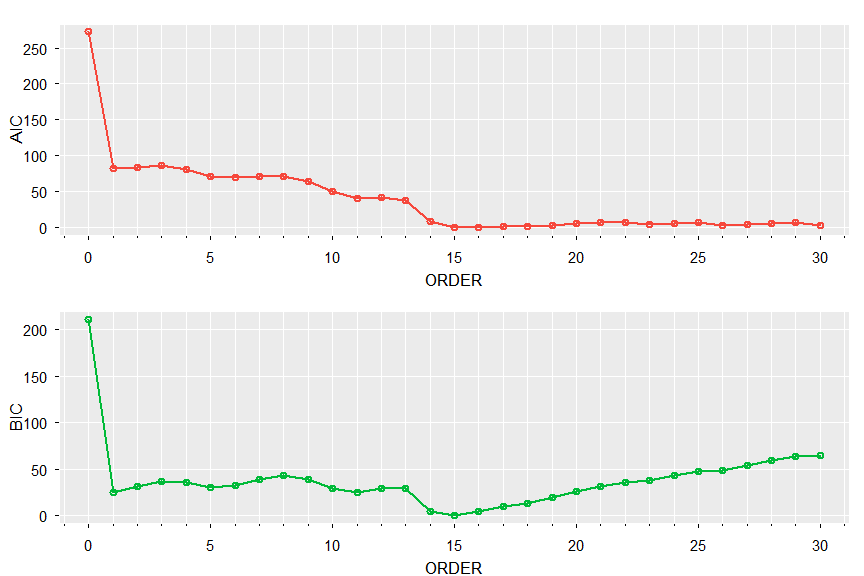

🔵 Based on BIC after detrending (default is using AIC with BIC=FALSE)

u <- spec.ic(soi, BIC=TRUE, detrend=TRUE, col=4, lwd=2)

🔵 Print and plot AIC and BIC (both pick order 15):

u[[1]] # notice the values are adjusted by the min

ORDER AIC BIC

[1,] 0 272.6937023 210.955320

[2,] 1 82.1484043 24.525915

[3,] 2 84.1441892 30.637592

[4,] 3 85.5926277 36.201922

[5,] 4 80.4715619 35.196749

[6,] 5 70.7822012 29.623280

[7,] 6 69.5898661 32.546837

[8,] 7 71.5718647 38.644728

[9,] 8 71.4320021 42.620757

[10,] 9 63.2815353 38.586183

[11,] 10 49.9872355 29.407775

[12,] 11 40.7220194 24.258451

[13,] 12 41.0928139 28.745138

[14,] 13 37.0833413 28.851557

[15,] 14 8.7779160 4.662024

[16,] 15 0.0000000 0.000000

[17,] 16 0.4321663 4.548058

[18,] 17 0.8834736 9.115258

[19,] 18 0.9605224 13.308199

[20,] 19 2.9348253 19.398394

[21,] 20 4.7475516 25.327012

[22,] 21 6.7012637 31.396616

[23,] 22 7.1553956 35.966641

[24,] 23 4.6428297 37.569967

[25,] 24 5.8610042 42.904033

[26,] 25 6.5000325 47.658954

[27,] 26 2.8918549 48.166668

[28,] 27 4.2581518 53.648857

[29,] 28 5.5960927 59.102690

[30,] 29 6.3765400 63.999030

[31,] 30 2.6978096 64.436191

tsplot(0:30, u[[1]][,2:3], type='o', col=2:3, xlab='ORDER', nxm=5, lwd=2, gg=TRUE)

more multivariate spectra

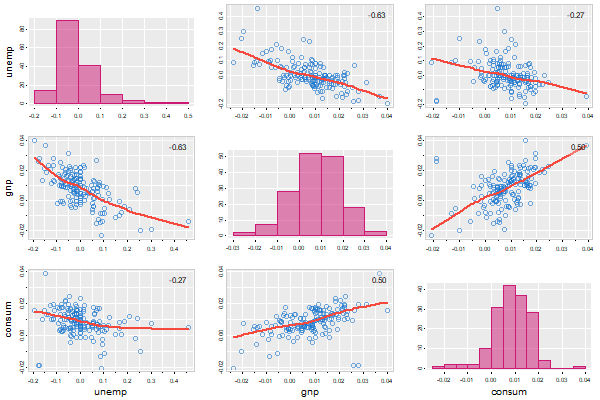

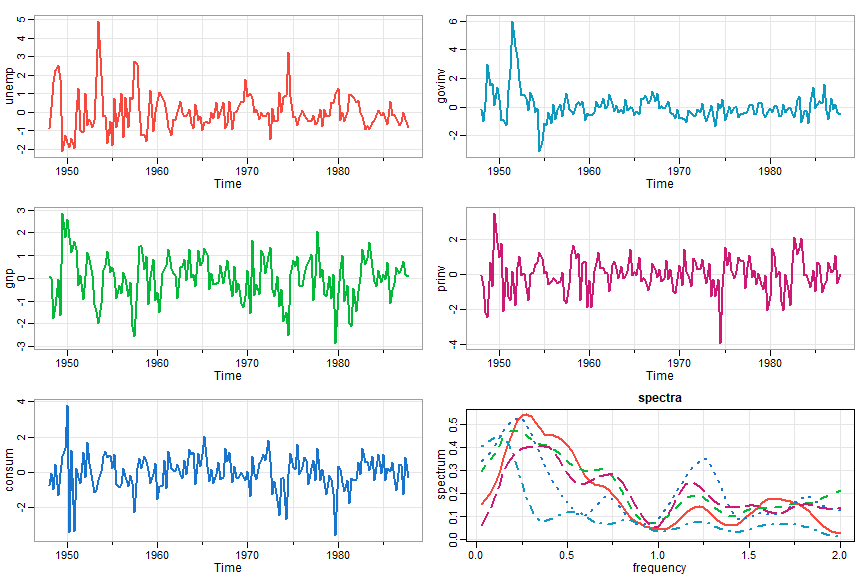

🔵 The data frame econ5 was used to consider the effect of quarterly GNP, consumption, and government and private investment on U.S. unemployment. In this case, mvspec will plot the individual spectra by default and you can extract the spectral matrices as fxx, an array of dimensions dim = c(p,p,nfreq) as well as plot coherencies and phases. Here, p = 5:

gr = diff(log(econ5))

gr = scale(gr) # for comparable spectra

tsplot(gr, ncol=2, col=2:6, lwd=2, byrow=FALSE, reset=FALSE)

gr.spec = mvspec(gr, spans=c(7,7), detrend=FALSE, taper=.25, col=2:6, lwd=2, main='spectra')

round(gr.spec$fxx, 2)

And a sample of the output of the last line giving the matrix estimate. The numbers at top refer to frequency ordinate:

, , 49

[,1] [,2] [,3] [,4] [,5]

[1,] 0.097+0.000i -0.048+0.042i -0.053+0.080i 0.032-0.037i -0.027+0.033i

[2,] -0.048-0.042i 0.129+0.000i 0.100-0.039i -0.052+0.012i 0.111+0.000i

[3,] -0.053-0.080i 0.100+0.039i 0.232+0.000i -0.041+0.001i 0.023+0.079i

[4,] 0.032+0.037i -0.052-0.012i -0.041-0.001i 0.051+0.000i -0.049+0.008i

[5,] -0.027-0.033i 0.111+0.000i 0.023-0.079i -0.049-0.008i 0.157+0.000i

, , 50

[,1] [,2] [,3] [,4] [,5]

[1,] 0.093+0.000i -0.054+0.045i -0.053+0.081i 0.030-0.034i -0.033+0.035i

[2,] -0.054-0.045i 0.124+0.000i 0.112-0.041i -0.048+0.010i 0.100+0.008i

[3,] -0.053-0.081i 0.112+0.041i 0.240+0.000i -0.034+0.009i 0.027+0.085i

[4,] 0.030+0.034i -0.048-0.010i -0.034-0.009i 0.050+0.000i -0.043+0.015i

[5,] -0.033-0.035i 0.100-0.008i 0.027-0.085i -0.043-0.015i 0.146+0.000i

6. Detecting Structural Breaks

autoSpec

Detection of Narrowband Frequency Changes in Time Series - the paper is here

💡 The basic idea is to fit local spectra by detecting slight changes in frequency. Section 2 of the paper on Resolution provides the motivation for the technique. If you haven’t guessed it already, the script is called

autoSpec()

and most of the inputs have default settings.

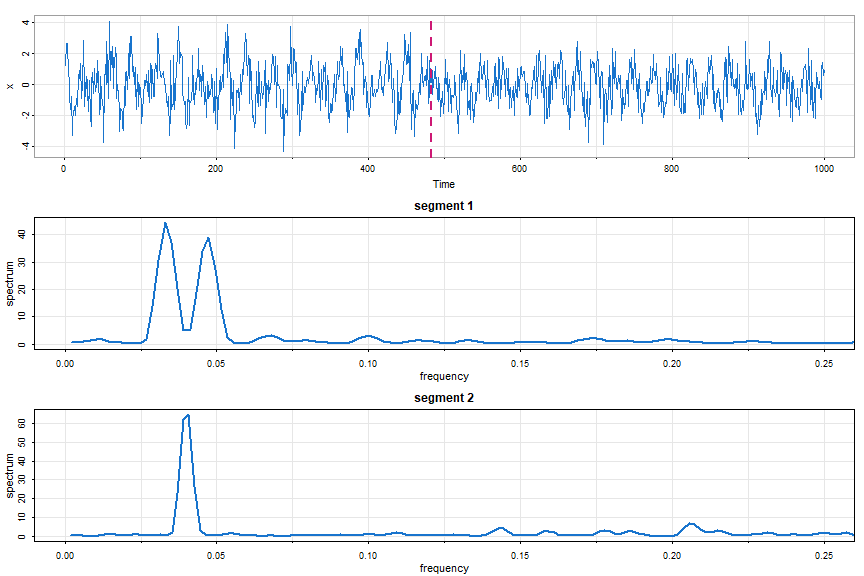

😎 Here’s an example where other techniques tend to fail (try it with autoParm below). A narrowband signal is modulated until halfway through.

Part of the input are min.freq and max.freq that specify the frequency range (min, max) over which to calculate the Whittle likelihood; the default is (0, ½), which is the entire frequency range.

# simulate data

set.seed(90210)

num = 500

t = 1:num

w = 2*pi/25

d = 2*pi/150

x1 = 2*cos(w*t)*cos(d*t) + rnorm(num)

x2 = cos(w*t) + rnorm(num)

x = c(x1, x2)

# periodogram (not shown) - all action below .1

mvspec(x)

autoSpec(x, max.freq=.1)

# returned breakpoints include the endpoints

# $breakpoints

# [1] 1 483 1000

#

# $number_of_segments

# [1] 2

#

# $segment_kernel_orders_m

# [1] 2 1

# plot everything

par(mfrow=c(3,1))

tsplot(x, col=4)

abline(v=483, col=6, lty=2, lwd=2)

mvspec(x[1:482], kernel=bart(2), taper=.5, main='segment 1', col=4, lwd=2, xlim=c(0,.25))

mvspec(x[483:1000], kernel=bart(1), taper=.5, main='segment 2', col=4, lwd=2, xlim=c(0,.25))

autoParm

Structural Break Estimation for Nonstationary Time Series Models. - the paper is here

💡 This is similar to autoSpec but fits local AR models. If you haven’t guessed it already, the script is called

autoParm()

and most of the inputs have default settings. Here’s an example.

##-- simulation - two AR(2)s that may look similar

x1 = sarima.sim(ar=c(1.69, -.81), n=500)

x2 = sarima.sim(ar=c(1.32, -.81), n=500)

x = c(x1, x2)

##-- but if you look at the data they're very different

##-- in fact, x2 is twice as fast as x1

tsplot(x)

##-- run procedure

autoParm(x)

# output

# returned breakpoints include the endpoints

# $breakpoints

# [1] 1 507 1000

#

# $number_of_segments

# [1] 2

#

# $segment_AR_orders

# [1] 2 2

##-- now fit AR(2)s to each piece

ar(x[1:506], order=2, aic=FALSE)

# Coefficients:

# 1 2

# 1.6786 -0.8085

# Order selected 2 sigma^2 estimated as 1.053

#

ar(x[507:1000], order=2, aic=FALSE)

# Coefficients:

# 1 2

# 1.2883 -0.7635

# Order selected 2 sigma^2 estimate as 1.144

7. Linearity Test

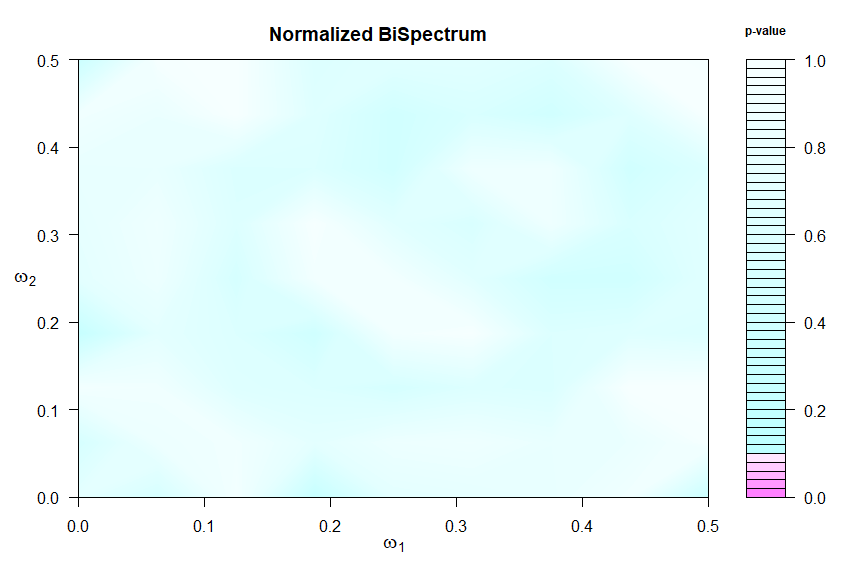

💡 Linear time series models are built on the linear process, where it is assumed that a univariate series Xt can be generated as

| Xt = μ + ∑ ψj Zt - j where ∑ | ψj | < ∞ |

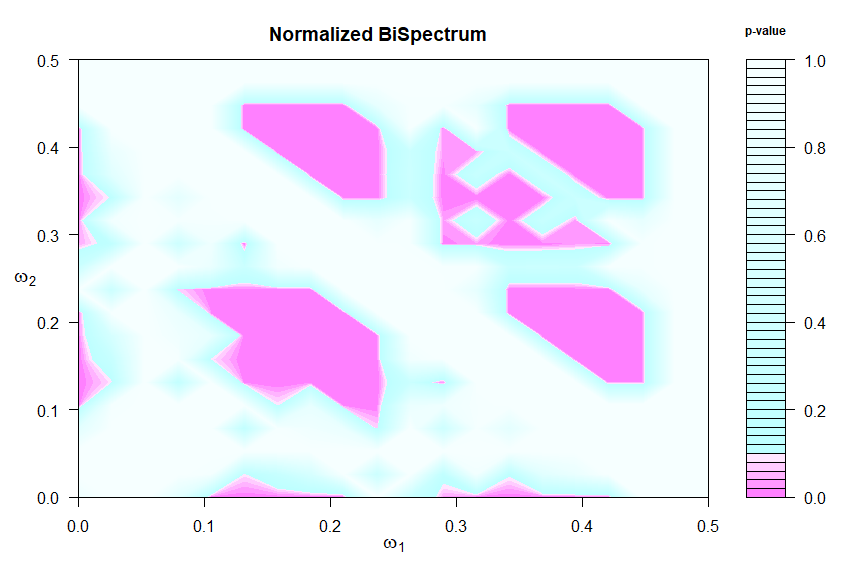

where Zt is a sequence of i.i.d. random variables with at least finite third moments. This assumption can be tested using the bispectrum, which is constant under the null hypothesis that the data are from a linear process with i.i.d. innovations. The workhorse here is

test.linear()

and more details can be found in its help file (?test.linear). Chi-squared test statistics are formed in blocks to measure departures from the null hypothesis and the corresponding p-values are displayed in a graphic and returned invisibly -

details in this paper.

🔵 First an example of a linear process where the graphic suggests a constant bispectrum.

test.linear(soi)

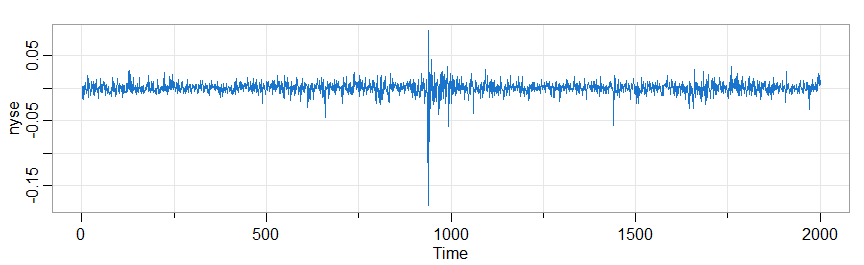

🔵 Notoriously nonlinear processes are financial series, for example the returns of the New York Stock Exchange (NYSE) from February 2, 1984 to December 31, 1991

# other packages have an 'nyse' data so to be safe we're setting

nyse = astsa::nyse # just to be sure

test.linear(nyse)

tsplot(nyse, col=4)

8. State Space Models

For Kalman filtering and smoothing the scripts are

KfilterandKsmooth

The default model (for both) is

♦ Version 1:

xt = Φ xt-1 + Υ ut + sQ wt and yt = At xt + Γ ut + sR vt,

where wt ~ iid Np(0, I) ⊥ vt ~ iid Nq(0, I) ⊥ x0 ~ Np(μ0, Σ0). In this case Q = sQ sQ’ and R = sR sR’. If it’s easier to model by specifying Q and/or R, you can use sQ = t(chol(Q)) or sQ = Q %^% .5 and so on.

There is an option to select the correlated errors version:

♦ Version 2:

xt+1 = Φ xt + Υ ut+1 + sQ wt, and yt = At xt + Γ ut + sR vt,

where cov(ws, vt) = S δst and so on.

❓ See the help files ?Kfilter and ?Ksmooth to see how the models are specified, but the calls look like

Kfilter(y, A, mu0, Sigma0, Phi, sQ, sR, Ups = NULL, Gam = NULL, input = NULL, S = NULL, version = 1).

The “always needed” stuff comes first, and the “sometimes needed” comes last. And again, if you want to model via Q and R, just use sQ = Q %^%.5 and sR = R %^%.5 [which works in the psd case] or sQ = t(chol(Q)) and sR = t(chol(R)) [which needs pd].

🔵 We’ll do the bootstrap example from the text, which used to take a long time… but now is fast.

# Example 6.13

tol = .0001 # determines convergence of optimizer

nboot = 500 # number of bootstrap replicates

# set up

y = window(qinfl, c(1953,1), c(1965,2)) # quarterly inflation

z = window(qintr, c(1953,1), c(1965,2)) # interest

num = length(y)

A = array(z, dim=c(1,1,num))

input = matrix(1,num,1)

# Function to Calculate Likelihood

Linn = function(para, y.data){ # pass parameters and data

phi = para[1]; alpha = para[2]

b = para[3]; Ups = (1-phi)*b

sQ = para[4]; sR = para[5]

kf = Kfilter(y.data, A, mu0, Sigma0, phi, sQ, sR, Ups, Gam=alpha, input) # version 1 by default

return(kf$like)

}

# Parameter ML Estimation

mu0 = 1

Sigma0 = .01

init.par = c(phi=.84, alpha=-.77, b=.85, sQ=.12, sR=1.1) # initial values

est = optim(init.par, Linn, NULL, y.data=y, method="BFGS", hessian=TRUE,

control=list(trace=1, REPORT=1, reltol=tol))

SE = sqrt(diag(solve(est$hessian)))

## results

phi = est$par[1]; alpha = est$par[2]

b = est$par[3]; Ups = (1-phi)*b

sQ = est$par[4]; sR = est$par[5]

round(cbind(estimate=est$par, SE), 3)

# output

### estimate SE

### phi 0.866 0.223

### alpha -0.686 0.486

### b 0.788 0.226

### sQ 0.115 0.107

### sR 1.135 0.147

# BEGIN BOOTSTRAP

# Run the filter at the estimates

kf = Kfilter(y, A, mu0, Sigma0, phi, sQ, sR, Ups, Gam=alpha, input)

# Pull out necessary values from the filter and initialize

xp = kf$Xp

Pp = kf$Pp

innov = kf$innov

sig = kf$sig

e = innov/sqrt(sig)

e.star = e # initialize values

y.star = y

xp.star = xp

k = 4:50 # hold first 3 observations fixed

para.star = matrix(0, nboot, 5) # to store estimates

init.par = c(.84, -.77, .85, .12, 1.1)

pb = txtProgressBar(min = 0, max = nboot, initial = 0, style=3) # progress bar

for (i in 1:nboot){

setTxtProgressBar(pb,i)

e.star[k] = sample(e[k], replace=TRUE)

for (j in k){

K = (phi*Pp[j]*z[j])/sig[j]

xp.star[j] = phi*xp.star[j-1] + Ups + K*sqrt(sig[j])*e.star[j]

}

y.star[k] = z[k]*xp.star[k] + alpha + sqrt(sig[k])*e.star[k]

est.star = optim(init.par, Linn, NULL, y.data=y.star, method='BFGS', control=list(reltol=tol))

para.star[i,] = cbind(est.star$par[1], est.star$par[2], est.star$par[3],

abs(est.star$par[4]), abs(est.star$par[5]))

}

close(pb)

# Some summary statistics

# SEs from the bootstrap

rmse = rep(NA,5)

for(i in 1:5){rmse[i]=sqrt(sum((para.star[,i]-est$par[i])^2)/nboot)

cat(i, rmse[i],"\n")

}

# output (compare these to the SEs above)

# 1 0.401331

# 2 0.5590043

# 3 0.3346493

# 4 0.1793103

# 5 0.2836505

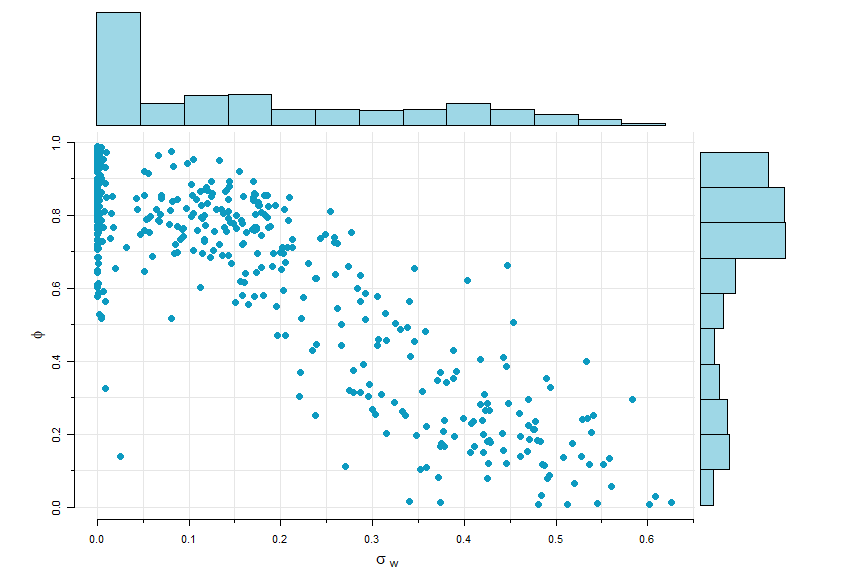

# Plot phi and sigw (scatter.hist in astsa)

phi = para.star[,1]

sigw = abs(para.star[,4])

phi = ifelse(phi<0, NA, phi) # any phi < 0 not plotted

scatter.hist(sigw, phi, ylab=expression(phi), xlab=expression(sigma[~w]),

hist.col=astsa.col(5,.4), pt.col=5, pt.size=1.5)

🔵 The smoother is similar. Here’s a simple example with no output shown.

# generate some data

set.seed(1)

sQ = 1; sR = 3; n = 100

mu0 = 0; Sigma0 = 10; x0 = rnorm(1,mu0,Sigma0)

w = rnorm(n); v = rnorm(n)

x = c(x0 + sQ*w[1]); y = c(x[1] + sR*v[1]) # initialize

for (t in 2:n){

x[t] = x[t-1] + sQ*w[t]

y[t] = x[t] + sR*v[t]

}

# let's make y a time series starting in the year 3000 just to mess with its mind

y = ts(y, start=3000)

# run and plot the filter

run = Ksmooth(y, A=1, mu0, Sigma0, Phi=1, sQ, sR)

# the smoother comes back as an array, so you have to un-array (drop) it

tsplot(cbind(y, drop(run$Xs)), spaghetti=TRUE, type='o', col=c(4,6), pch=c(1,NA))

legend('topleft', legend=c("y(t)","Xs(t)"), lty=1, col=c(4,6), bty="n", pch=c(1,NA))

Beginners Paradise

💡 There is a basic linear state space model script in astsa :

ssm()

🔵 For a univariate model (both $p=q=1$), write the states as xt and the observations as yt.

xt = α + φ xt-1 + wt and yt = A xt + vt

where wt ~ iid N(0, σw) ⊥ vt ~ iid N(0, σv) ⊥ x0 ~ N(μ0, σ0)

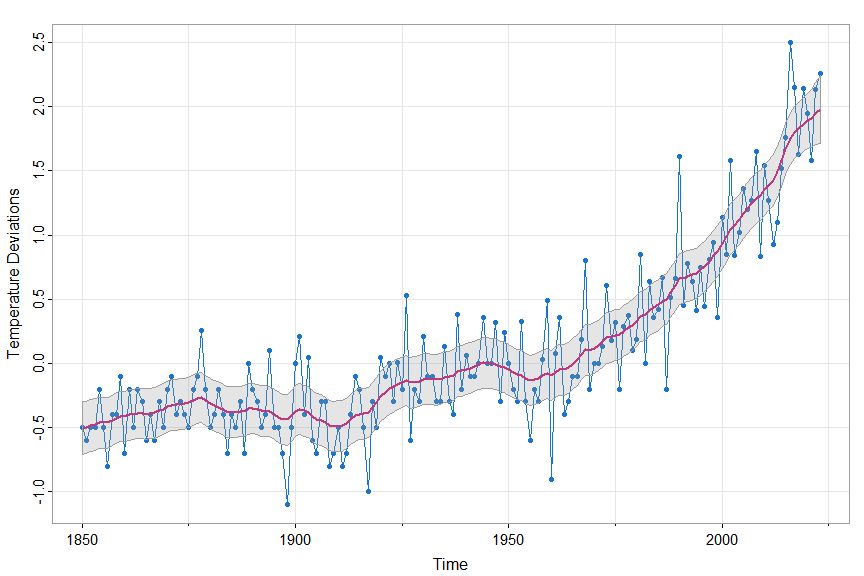

🔵 We’ll fit the model to one of the global temperature series. To use the script, you have to give initial estimates and then the script fits the model via MLE. The initial values of μ0 and σ0 are chosen automatically. In this example, we hold φ fixed at 1.

u = ssm(gtemp_land, A=1, phi=1, alpha=.01, sigw=.01, sigv=.1, fixphi=TRUE)

(remove the fixphi=TRUE to estimate φ) with output:

estimate SE

alpha 0.01428210 0.005138887

sigw 0.06643393 0.013368981

sigv 0.29494720 0.017370440

and a nice picture - the data [yt], the smoothers [ E(xt | y1 ,…, yn) ] and ±2 root MSPEs. The smoothers are

in Xs and the MSPEs are in Ps:

tsplot(gtemp_land, col=4, type="o", pch=20, ylab="Temperature Deviations")

lines(u$Xs, col=6, lwd=2)

xx = c(time(u$Xs), rev(time(u$Xs)))

yy = c(u$Xs-2*sqrt(u$Ps), rev(u$Xs+2*sqrt(u$Ps)))

polygon(xx, yy, border=8, col=gray(.6, alpha=.25) )

🔵 The output of ssm() gives the predictors [Xp] and MSPE [Pp], the

filtered values [Xf and Pf] and the smoothers [Xs and Ps]:

str(u)

List of 6

$ Xp: Time-Series [1:174] from 1850 to 2023: -0.446 -0.445 -0.467 -0.46 -0.454 ...

$ Pp: Time-Series [1:174] from 1850 to 2023: 0.0292 0.0263 0.0246 0.0236 0.023 ...

$ Xf: Time-Series [1:174] from 1850 to 2023: -0.459 -0.481 -0.474 -0.468 -0.401 ...

$ Pf: Time-Series [1:174] from 1850 to 2023: 0.0218 0.0202 0.0192 0.0186 0.0182 ...

$ Xs: Time-Series [1:174] from 1850 to 2023: -0.503 -0.497 -0.487 -0.475 -0.463 ...

$ Ps: Time-Series [1:174] from 1850 to 2023: 0.01094 0.01051 0.01023 0.01005 0.00994 ...

9. EM Algorithm and Missing Data

💡 To use the EM algorithm presented in Shumway & Stoffer (1982) and discussed in detail in Chapter 6 of the text Time Series Analysis and Its Applications: With R Examples, use the script

EM()

The call looks like

EM(y, A, mu0, Sigma0, Phi, Q, R, Ups=NULL, Gam=NULL, input=NULL, max.iter=100, tol=1e-04)

and sort of mimics the Kfilter and Ksmooth calls but accepts Q and R directly. However, the code only works with the uncorrelated noise script (version 1).

🔵 Here’s a simple univariate example. With y = gtemp_land, the model we’ll fit is

xt = α + φ xt-1 + wt and yt = A xt + vt

where wt ~ iid N(0, σw) ⊥ vt ~ iid N(0, σv) ⊥ x0 ~ N(μ0, σ0)

y = gtemp_land

A = 1 # if A is constant, enter it that way

Ups = 0.01 # alpha

Phi = 1

Q = 0.001 # notice you input Q

R = 0.01 # and R now

mu0 = mean(y[1:5]) # this is how ssm() chooses

Sigma0 = var(jitter(y[1:5])) # initial state values

input = rep(1, length(y))

( em = EM(y, A, mu0, Sigma0, Phi, Q, R, Ups, Gam=NULL, input) )

with partial output

$Phi

[1] 1.024571

$Q

[,1]

[1,] 0.001541975

$R

[,1]

[1,] 0.0941836

$Ups

[1] 0.01301747

$Gam

NULL

$mu0

[,1]

[1,] -0.5036954

$Sigma0

[,1]

[1,] 0.001961116

$like

[1] 328.3526 -110.5628 -112.3838 -112.3874

$niter

[1] 4

$cvg

[1] 3.194832e-05

🔵 Missing data can be entered as NA or zero (0) in the data (y) and measurement matrices (At). Next, we’ll do a missing data example, blood, which contains the daily blood work of a patient for 91 days and where there are many missing observations after the first month.

tsplot(blood, type='o', col=c(6,4,2), lwd=2, pch=19, cex=1)

- First the set up.

xt = Φ xt-1 + wt and yt = At xt + vt

where At is 3x3 identity when observed, and 0 matrix when missing. The errors are wt ~ iid N3(0, Q) ⊥ vt ~ iid N3(0, V) ⊥ x0 ~ N3(μ0, Σ0).

y = blood # missing values are NA

num = nrow(y)

A = array(0, dim=c(3,3,num)) # creates num 3x3 zero matrices

for(k in 1:num) if (!is.na(y[k,1])) A[,,k]= diag(1,3) # measurement matrices for observed

- Next, run the EM Algorithm by specifying model parameters. You can specify the max number of iterations and relative tolerance, too.

# Initial values

mu0 = matrix(0,3,1)

Sigma0 = diag(c(.1,.1,1) ,3)

Phi = diag(1, 3)

Q = diag(c(.01,.01,1), 3)

R = diag(c(.01,.01,1), 3)

# Run EM

(em = EM(y, A, mu0, Sigma0, Phi, Q, R))

The (partial) output is (NOTE: the output used to start at iteration 1, but after version 2.4 was published, we decided to start at 0 because the first evaluation of the likelihood is at the initial values … right now, it’s only this way on GitHub)

iteration -loglikelihood

0 68.28328

1 -183.9361

2 -194.2051

3 -197.5444

4 -199.7442

5 -201.6431

. .

60 -233.2501

61 -233.2837

62 -233.3121

63 -233.3357

64 -233.3545

# estimates below

$Phi

[,1] [,2] [,3]

[1,] 0.98395673 -0.03975976 0.008688178

[2,] 0.05726606 0.92656284 0.006023044

[3,] -1.26586175 1.96500888 0.820475630

$Q

[,1] [,2] [,3]

[1,] 0.013786286 -0.001974193 0.01147321

[2,] -0.001974193 0.002796296 0.02685780

[3,] 0.011473214 0.026857800 3.33355946

$R

[,1] [,2] [,3]

[1,] 0.00694027 0.00000000 0.0000000

[2,] 0.00000000 0.01707764 0.0000000

[3,] 0.00000000 0.00000000 0.9389751

$mu0

[,1]

[1,] 2.137368

[2,] 4.417385

[3,] 25.815731

$Sigma0

[,1] [,2] [,3]

[1,] 2.910997e-04 -4.161189e-05 0.0002346656

[2,] -4.161189e-05 1.923713e-04 -0.0002854434

[3,] 2.346656e-04 -2.854434e-04 0.1052641500

$like

[1] 68.28328 -183.93608 -194.20508 -197.54440 -199.74425 -201.64313 -203.42258 -205.12530

[9] -206.75951 -208.32511 -209.82091 -211.24639 -212.60202 -213.88906 -215.10935 -216.26514

[17] -217.35887 -218.39311 -219.37048 -220.29354 -221.16485 -221.98686 -222.76196 -223.49243

[25] -224.18049 -224.82824 -225.43771 -226.01085 -226.54953 -227.05552 -227.53054 -227.97621

[33] -228.39410 -228.78569 -229.15242 -229.49563 -229.81661 -230.11659 -230.39674 -230.65816

[41] -230.90189 -231.12893 -231.34021 -231.53662 -231.71899 -231.88811 -232.04473 -232.18954

[49] -232.32321 -232.44634 -232.55954 -232.66333 -232.75824 -232.84475 -232.92332 -232.99437

[57] -233.05831 -233.11551 -233.16633 -233.21110 -233.25013 -233.28372 -233.31215 -233.33567

[65] -233.35454

$niter

[1] 64

$cvg

[1] 8.086056e-05 # relative tolerance of -loglikelihood at convergence

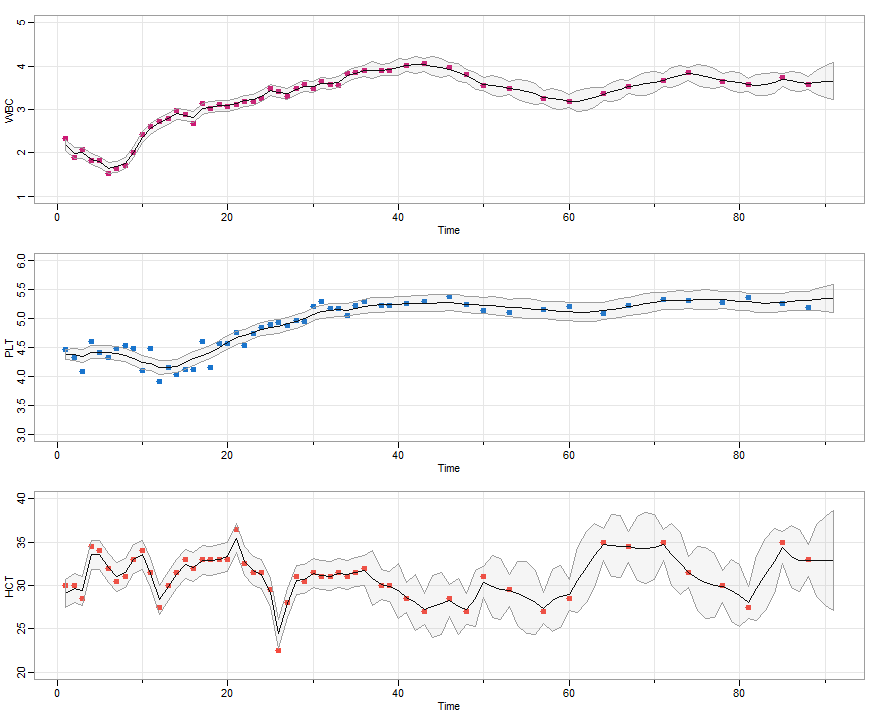

- Now plot the results.

# Run smoother at the estimates (using the new Ksmooth script)

sQ = em$Q %^% .5

sR = sqrt(em$R)

ks = Ksmooth(y, A, em$mu0, em$Sigma0, em$Phi, sQ, sR)

# Pull out the values

y1s = ks$Xs[1,,]

y2s = ks$Xs[2,,]

y3s = ks$Xs[3,,]

p1 = 2*sqrt(ks$Ps[1,1,])

p2 = 2*sqrt(ks$Ps[2,2,])

p3 = 2*sqrt(ks$Ps[3,3,])

# plots

par(mfrow=c(3,1))

tsplot(WBC, type='p', pch=19, ylim=c(1,5), col=6, lwd=2, cex=1)

lines(y1s)

xx = c(time(WBC), rev(time(WBC))) # same for all

yy = c(y1s-p1, rev(y1s+p1))

polygon(xx, yy, border=8, col=astsa.col(8, alpha = .1))

tsplot(PLT, type='p', ylim=c(3,6), pch=19, col=4, lwd=2, cex=1)

lines(y2s)

yy = c(y2s-p2, rev(y2s+p2))

polygon(xx, yy, border=8, col=astsa.col(8, alpha = .1))

tsplot(HCT, type='p', pch=19, ylim=c(20,40), col=2, lwd=2, cex=1)

lines(y3s)

yy = c(y3s-p3, rev(y3s+p3))

polygon(xx, yy, border=8, col=astsa.col(8, alpha = .1))

🤓 EM with Parameter Constraints

💡 The script doesn’t allow constraints on the parameters, but constrained parameter estimation can be accomplished by being a little clever. We demonstrate by fitting an AR(2) with noise.

The model is

xt = φ1 xt-1 + φ2 xt-2 + wt and yt = xt + vt.

or in state-space form

\[\begin{pmatrix}x_t\cr x_{t-1}\end{pmatrix} = \begin{bmatrix}\phi_1 & \phi_2\cr 1 & 0\end{bmatrix}\begin{pmatrix}x_{t-1}\cr x_{t-2}\end{pmatrix} + \begin{pmatrix}w_{t}\cr 0\end{pmatrix}\] \[y_t = \begin{bmatrix}1 & 0\end{bmatrix} \begin{pmatrix}x_t\cr x_{t-1}\end{pmatrix} + v_t\]Here we go

# generate some data

set.seed(1)

num = 100

phi1 = 1.5; phi2 =-.75 # the ar parameters

Phi= diag(0,2)

Phi[1,1] = phi1; Phi[1,2] = phi2

Phi[2,1] = 1

Q = diag(0, 2)

Q[1,1] = 1 # var(w[t])

# simulate the AR(2) states (var w[t] is 1 by default)

x = sarima.sim(ar = c(phi1, phi2), n=num)

# the observations

A = cbind(1, 0)

R = .01 # var(v[t])

y = x + rnorm(num, 0, sqrt(R))

# fix the initial values throughout

mux = rbind(0, 0)

Sigmax = matrix(c(8.6,7.4,7.4,8.6), 2,2)

# for estimation, use these not so great starting values

Phi[1,1]=.1 ; Phi[1,2]=.1

Q[1,1] = .1

R = .1

###########################################################

#### run EM one at a time, then re-constrain the parms ####

###########################################################

###-- with some extra coding, the loop can be stopped when a given

###-- tolerance is reached by monitoring em$like at each iteration ...

for (i in 1:75){

em = EM(y, A, mu0=mux, Sigma0=Sigmax, Phi, Q, R, max.iter = 1)

Phi= diag(0,2)

Phi[2,1] = 1

Phi[1,1] = em$Phi[1,1]; Phi[1,2] = em$Phi[1,2]

Q = diag(0, 2)

Q[1,1] = em$Q[1,1]

R = em$R

}

# ### some output ###

# Note that the iteration output used to start at 1,

# but now it more precisely starts at 0

#

#iteration -loglikelihood

# 0 1485.486

#iteration -loglikelihood

# 0 95.26131

#iteration -loglikelihood

# 0 73.45769

#iteration -loglikelihood

# 0 63.83681

#iteration -loglikelihood

# 0 58.44693

# . .

# . .

#iteration -loglikelihood

# 0 48.69579

#iteration -loglikelihood

# 0 48.69518

#iteration -loglikelihood

# 0 48.6946

#iteration -loglikelihood

# 0 48.69405

############################

## Results

Phi # (actual 1.5 and -.75)

## [,1] [,2]

## [1,] 1.513079 -0.737669

## [2,] 1.000000 0.000000

Q # (actual 1)

## [,1] [,2]

## [1,] 0.7973415 0

## [2,] 0.0000000 0

R # (actual .01)

## [,1]

## [1,] 0.04462222

😎 And that’s how it’s done.

10. Bayesian Techniques

💡 We’ve added some scripts to handle Bayesian analysis. So far we have

ar.mcmcto fit AR models

SV.mcmcto fit stochastic volatility models

ffbsthe forward filter backward sampling (FFBS) algorithm - part of Gibbs for LINEAR SS models

AR Models

🔵 For a minimal example, we’ll fit an AR(2) to the Recruitment (rec) data.

xt = φ0 + φ1 xt-1 + φ2 xt-2 + σ wt

where wt is standard Gaussian white noise.

You just need to input the data and the order because the priors, the number of MCMC iterations (including burnin) have defaults. The method is fast and efficient. The output includes a graphic (unless plot = FALSE) and some quantiles of the sampled parameters. For further details and references, see the help file (?ar.mcmc).

u = ar.mcmc(rec, 2)

with screen output

Quantiles:

phi0 phi1 phi2 sigma

1% 3.991699 1.268724 -0.5604687 8.799926

2.5% 4.504180 1.276576 -0.5460294 8.903435

5% 4.897493 1.289001 -0.5306669 9.001894

10% 5.312776 1.302280 -0.5163514 9.109764

25% 5.976938 1.325613 -0.4907099 9.291095

50% 6.780525 1.353442 -0.4614311 9.498246

75% 7.571304 1.380684 -0.4361400 9.703718

90% 8.235147 1.406633 -0.4130296 9.913079

95% 8.643331 1.424673 -0.3985069 10.018678

97.5% 8.928998 1.435397 -0.3874075 10.130158

99% 9.482394 1.458155 -0.3751349 10.335975

and graphics (now uses tspairs)

The draws are returned invisibly:

head(u)

# phi0 phi1 phi2 sigma

# [1,] 6.414775 1.353891 -0.4498024 9.055021

# [2,] 8.140380 1.417450 -0.5423222 9.631700

# [3,] 6.251149 1.381373 -0.4903105 9.012220

# [4,] 5.635571 1.324994 -0.4188650 10.144267

# [5,] 8.116873 1.344782 -0.4676563 8.994929

# [6,] 6.118467 1.312165 -0.4166178 9.362385

Gibbs Sampling for Linear State Space Models

🔵 The package has an ffbs script (Forward Filtering Backward Sampling - FFBS)

to facilitate Gibbs sampling for linear state space models:

xt = Φ xt-1 + Υ ut + sQ wt, yt = At xt + Γ ut + sR vt,

wt ~ iid Np(0, I) ⊥ vt ~ iid Nq(0, I) ⊥ x0 ~ Np(μ0, Σ0) and ut is an r-dimensional input sequence.

If $\Theta$ represents the parameters, $x_{0:n}$ the states, $y_{1:n}$ the data, then the generic Gibbs sampler is (rinse and repeat)

(1) sample $\Theta’ \sim p(\Theta \mid x_{0:n}, y_{1:n})$

(2) sample $x_{0:n}’ \sim p(x_{0:n} \mid \Theta’, y_{1:n})$

ffbs accomplishes (2). There is NOT a script to do (1) because the model is too general to build a decent script to cover the possibilities. The script uses version 1 of Kfilter and Ksmooth.

🛂 Example: Local Level Model

xt = xt-1 + wt and yt = xt + 3 vt

where wt and vt are independent standard Gaussian noise.

# generate some data from the model

set.seed(1)

sQ = 1; sR = 3 # 2 parameters

mu0 = 0; Sigma0 = 10; x0 = rnorm(1,mu0,Sigma0) # initial state

n = 100; w = rnorm(n); v = rnorm(n)

x = c(x0 + sQ*w[1]) # initialize states

y = c(x[1] + sR*v[1]) # initialize obs

for (t in 2:n){

x[t] = x[t-1] + sQ*w[t]

y[t] = x[t] + sR*v[t]

}

# we'll plot these below

# set up the Gibbs sampler

burn = 50; n.iter = 1000

niter = burn + n.iter

draws = c()

# priors for R (a,b) and Q (c,d) IG distributions

a = 2; b = 2; c = 2; d = 1

###-- (1) initialize - sample sQ and sR --###

sR = sqrt(1/rgamma(1,a,b))

sQ = sqrt(1/rgamma(1,c,d))

# progress bar

pb = txtProgressBar(min = 0, max = niter, initial = 0, style=3)

# run it

for (iter in 1:niter){

###-- (2) sample the states --###

run = ffbs(y,A=1,mu0=0,Sigma0=10,Phi=1,sQ,sR)

###-- (1) sample the parameters --###

xs = as.matrix(run$Xs)

R = 1/rgamma(1, a+n/2, b+sum((y-xs)^2)/2)

sR = sqrt(R)

Q = 1/rgamma(1, c+(n-1)/2, d+sum(diff(xs)^2)/2)

sQ = sqrt(Q)

## store everything

draws = rbind(draws,c(sQ,sR,xs))

setTxtProgressBar(pb, iter)

}

close(pb)

# pull out the results for easy plotting

draws = draws[(burn+1):(niter),]

q025 = function(x){quantile(x,0.025)}

q975 = function(x){quantile(x,0.975)}

xs = draws[,3:(n+2)]

lx = apply(xs,2,q025)

mx = apply(xs,2,mean)

ux = apply(xs,2,q975)

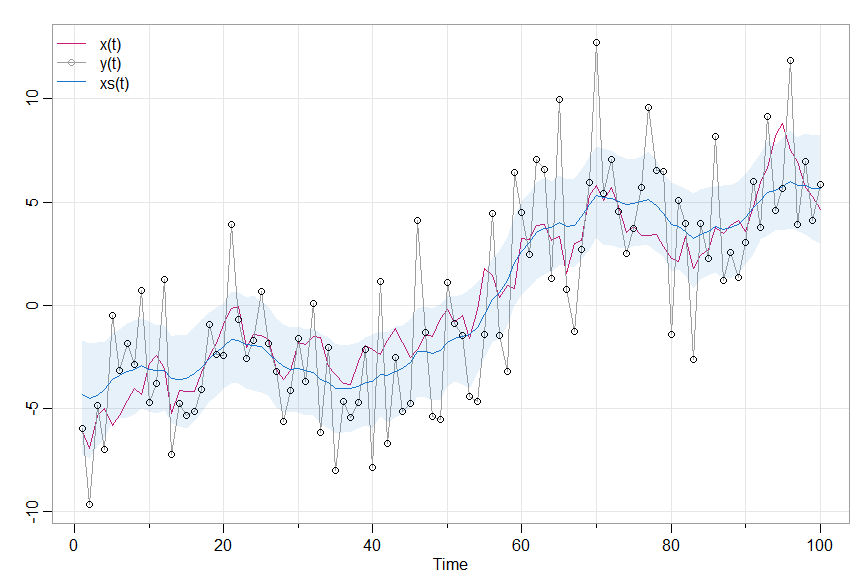

# some graphics

tsplot(cbind(x,y,mx), spag=TRUE, ylab='', col=c(6,8,4), lwd=c(1,1,1.5), type='o', pch=c(NA,1,NA))

legend('topleft', legend=c("x(t)","y(t)","xs(t)"), lty=1, col=c(6,8,4), lwd=1.5, bty="n", pch=c(NA,1,NA))

points(y)

xx=c(1:100, 100:1)

yy=c(lx, rev(ux))

polygon(xx, yy, border=NA, col=astsa.col(4,.1))

# and the parameters

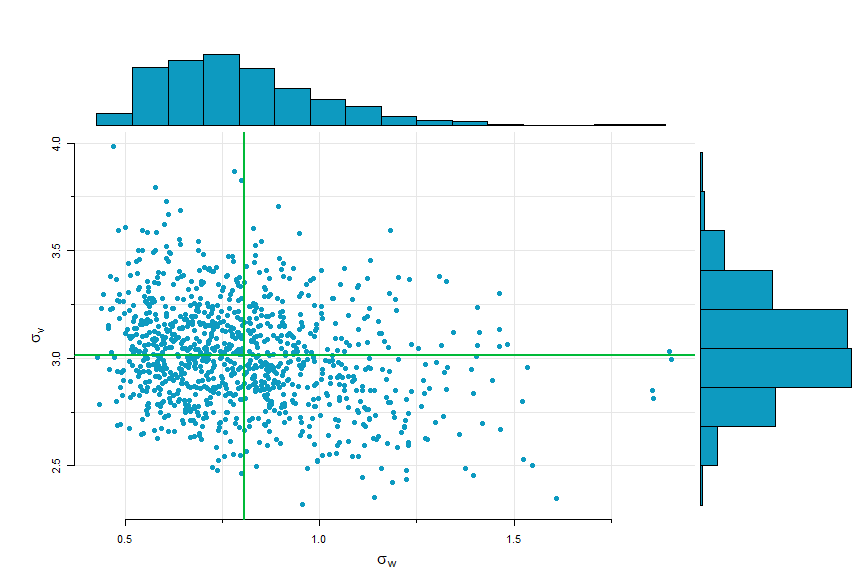

scatter.hist(draws[,1],draws[,2], xlab=expression(sigma[w]), ylab=expression(sigma[v]),

reset.par = FALSE, pt.col=5, hist.col=5)

abline(v=mean(draws[,1]), col=3, lwd=2)

abline(h=mean(draws[,2]), col=3, lwd=2)

🛂 Example: Structural Model

Here’s the model and some discussion. $y_t = \text{jj}$ (Johnson & Johnson data), $T_t$ is trend and $S_t$ is quarterly season and

$y_t = T_t + S_t + v_t$ where $T_t = \phi T_{t-1} + w_{t1}$ and $S_t+S_{t-1}+S_{t-2}+S_{t-3} = w_{t2}$.

The set up (Example 6.26 in edition 5 of the text for more details):

y = jj # the data

### setup - model and initial parameters

set.seed(90210)

n = length(y)

A = matrix(c(1,1,0,0), 1, 4)

Phi = diag(0,4)

Phi[1,1] = 1.03

Phi[2,] = c(0,-1,-1,-1); Phi[3,]=c(0,1,0,0); Phi[4,]=c(0,0,1,0)

mu0 = rbind(.7,0,0,0)

Sigma0 = diag(.04, 4)

sR = 1 # observation noise standard deviation

sQ = diag(c(.1,.1,0,0)) # state noise standard deviations on the diagonal

### initializing and hyperparameters

burn = 50

n.iter = 1000

niter = burn + n.iter

draws = NULL

a = 2; b = 2; c = 2; d = 1 # hypers (c and d for both Qs)

pb = txtProgressBar(min = 0, max = niter, initial = 0, style=3) # progress bar

### start Gibbs

for (iter in 1:niter){

# draw states

run = ffbs(y,A,mu0,Sigma0,Phi,sQ,sR) # initial values are given above

xs = run$Xs

# obs variance

R = 1/rgamma(1,a+n/2,b+sum((as.vector(y)-as.vector(A%*%xs[,,]))^2))

sR = sqrt(R)

# beta where phi = 1+beta

Y = diff(xs[1,,])

D = as.vector(lag(xs[1,,],-1))[-1]

regu = lm(Y~0+D) # est beta = phi-1

phies = as.vector(coef(summary(regu)))[1:2] + c(1,0) # phi estimate and SE

dft = df.residual(regu)

Phi[1,1] = phies[1] + rt(1,dft)*phies[2] # use a t to sample phi

# state variances

u = xs[,,2:n] - Phi%*%xs[,,1:(n-1)]

uu = u%*%t(u)/(n-2)

Q1 = 1/rgamma(1,c+(n-1)/2,d+uu[1,1]/2)

sQ1 = sqrt(Q1)

Q2 = 1/rgamma(1,c+(n-1)/2,d+uu[2,2]/2)

sQ2 = sqrt(Q2)

sQ = diag(c(sQ1, sQ2, 0,0))

# store results

trend = xs[1,,]

season= xs[2,,]

draws = rbind(draws,c(Phi[1,1],sQ1,sQ2,sR,trend,season))

setTxtProgressBar(pb,iter)

}

close(pb)

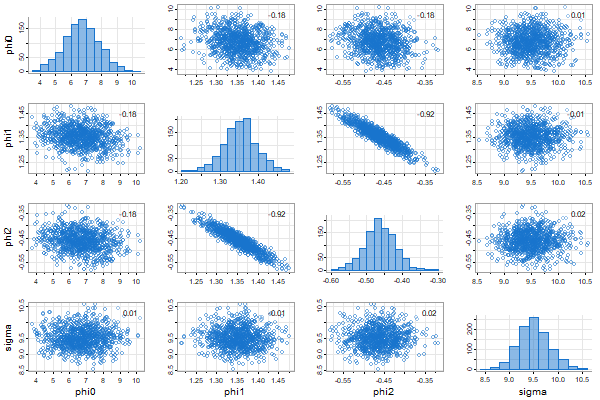

##- display results -##

# set up

u = draws[(burn+1):(niter),]

parms = u[,1:4]

q025 = function(x){quantile(x,0.025)}

q975 = function(x){quantile(x,0.975)}

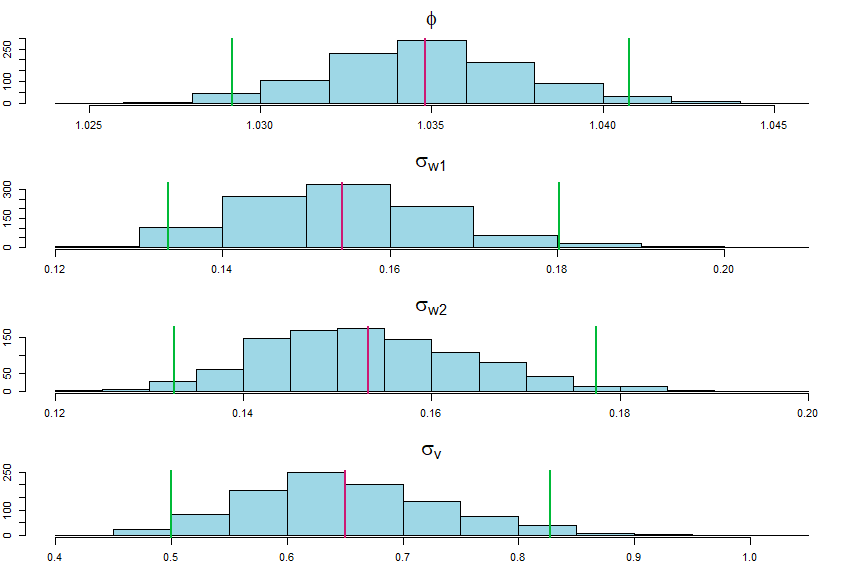

## plot parameters (display at end)

names= c(expression(phi), expression(sigma[w1]), expression(sigma[w2]), expression(sigma[v]))

par(mfrow=c(4,1), mar=c(2,1,2,1)+1)

for (i in 1:4){

hist(parms[,i], col=astsa.col(5,.4), main=names[i], xlab='', cex.main=2)

u1 = apply(parms,2,q025); u2 = apply(parms,2,mean); u3 = apply(parms,2,q975);

abline(v=c(u1[i],u2[i],u3[i]), lwd=2, col=c(3,6,3))

}

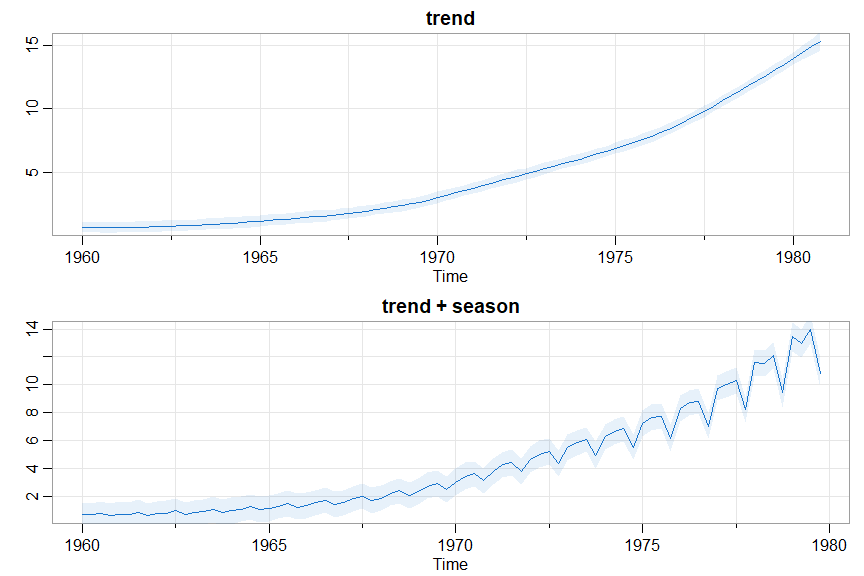

### plot states (display at end)

# trend

dev.new()

par(mfrow=2:1)

tr = ts(u[,5:(n+4)], start=1960, frequency=4)

ltr = ts(apply(tr,2,q025), start=1960, frequency=4)

mtr = ts(apply(tr,2,mean), start=1960, frequency=4)

utr = ts(apply(tr,2,q975), start=1960, frequency=4)

tsplot(mtr, ylab='', col=4, main='trend')

xx=c(time(mtr), rev(time(mtr)))

yy=c(ltr, rev(utr))

polygon(xx, yy, border=NA, col=astsa.col(4,.1))

# trend + season

sea = ts(u[,(n+5):(2*n)], start=1960, frequency=4)

lsea = ts(apply(sea,2,q025), start=1960, frequency=4)

msea = ts(apply(sea,2,mean), start=1960, frequency=4)

usea = ts(apply(sea,2,q975), start=1960, frequency=4)

tsplot(msea+mtr, ylab='', col=4, main='trend + season')

xx=c(time(msea), rev(time(msea)))

yy=c(lsea+ltr, rev(usea+utr))

polygon(xx, yy, border=NA, col=astsa.col(4,.1))

🎵 And let’s check the efficiency of the sampler ( see ESS ); recall niter = 1000.

colnames(parms)=c('Phi11','sQ1','sQ2','sR')

apply(parms,2,ESS)

Phi11 sQ1 sQ2 sR

571.0002 1000.0000 1000.0000 270.7789

# and maybe look at some other things (not displayed)

tsplot(parms, col=4, ncolm=2) # plot the traces

acfm(parms) # view the ACFs

ESS

🐷 The effective sample size (ESS) is a measure of efficiency of an MCMC procedure based on estimating a posterior mean. The package now includes a script to estimate ESS given a sequence of samples. It was used in the display for the Stochastic Volatility example and just above in the structural equation model.

Here’s another example.

# Fit an AR(2) to the Recruitment series

u = ar.mcmc(rec, 2, n.iter = 1000, plot = FALSE)

# Quantiles:

# phi0 phi1 phi2 sigma

# 1% 4.198 1.256 -0.5601 8.875

# 2.5% 4.640 1.274 -0.5459 8.937

# . . .

# then calculate the ESSs

apply(u, 2, ESS)

phi0 phi1 phi2 sigma

1000 1000 1000 1000

# nice

11. Stochastic Volatility Models

👯astsa has classical and Bayesian versions …

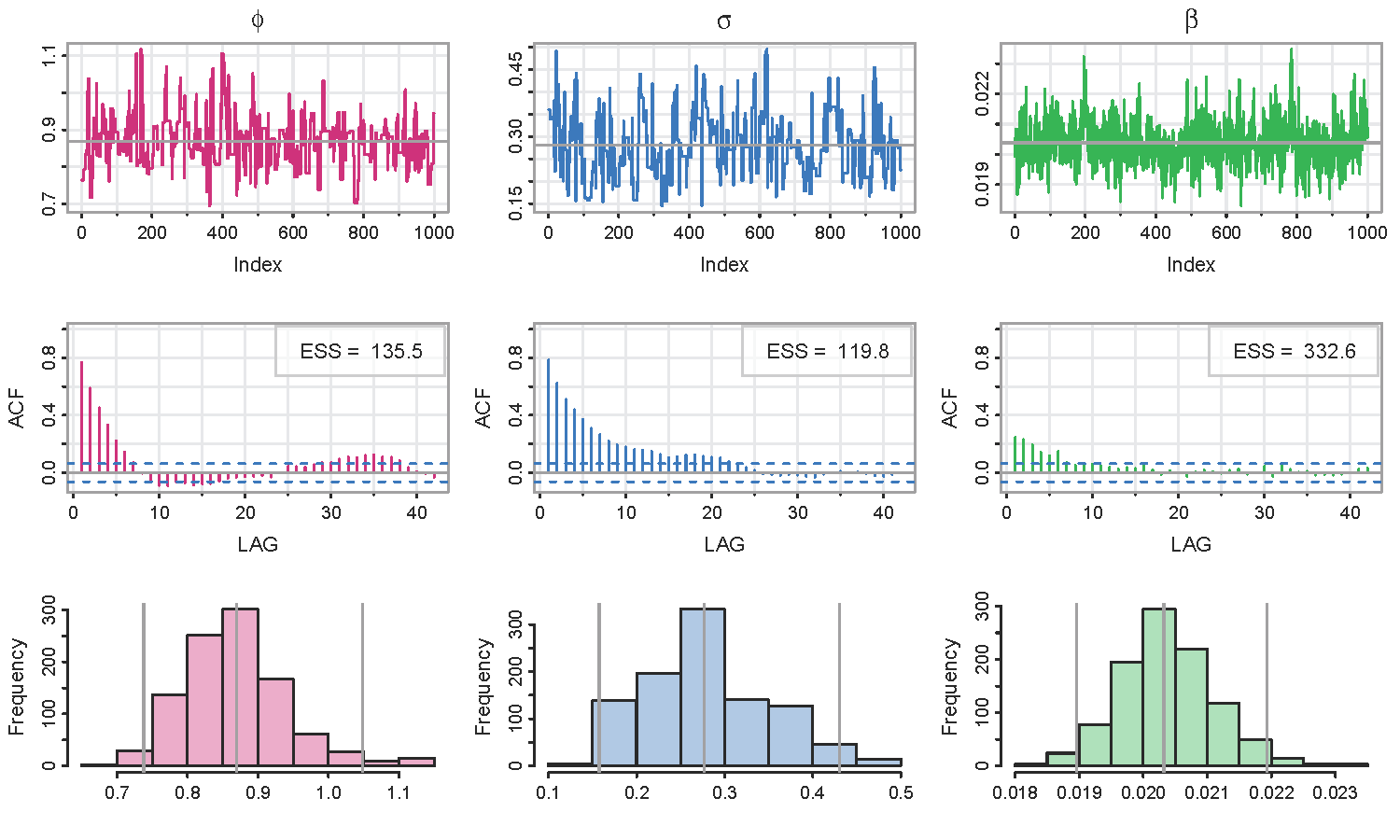

Bayesian:

🔵 For an example, we’ll fit a stochastic volatility model to the S&P500 weekly returns(sp500w). We’ve also added some new financial data sets, sp500.gr (daily S&P 500 returns) and BCJ (daily returns for 3 banks, Bank of America, Citi, and JP Morgan Chase). The model is

xt = φ xt-1 + σ wt , and yt =β exp (½ xt) εt

where wt and εt are independent standard Gaussian white noise, xt is the hidden log-volatility process and yt are the returns. Most of the inputs have defaults, so a minimal run just needs the data specified.

u = SV.mcmc(sp500w) # put the results in an object - it's important

The immediate output shows the status, then the time to run and the acceptance rate of the Metropolis MCMC (which should be close to 28%):

|= = = = = = = = = = = = = = = = = = = = = = = = =| 100%

Time to run (secs):

user system elapsed

42.02 0.71 44.73

The acceptance rate is: 29.7%

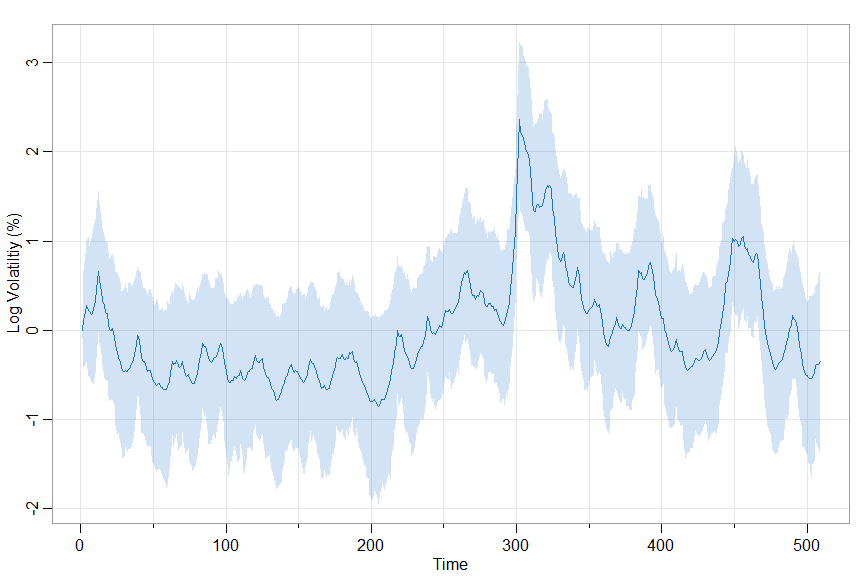

and graphics (traces, effective sample sizes, ACFs, histograms with 2.5%-50%-97.5% quantiles followed by the posterior mean log-volatility with 95% credible intervals).

🐩 The Effective Sample Size (ESS) in the graphic above were calculated using the script ESS.

An easy way to see the defaults (a list of options) is to look at the structure of the object:

str(u)

List of 5

$ phi : num [1:1000] 0.764 0.764 0.764 0.764 0.764 ...

$ sigma : num [1:1000] 0.36 0.36 0.36 0.36 0.36 ...

$ beta : num [1:1000] 0.0199 0.0206 0.0208 0.0202 0.0208 ...

$ log.vol: num [1:1000, 1:509] 0.0146 0.0266 -0.0694 -0.1368 -0.0442 ...

$ options:List of 8

..$ nmcmc : num 1000

..$ burnin : num 100

..$ init : num [1:3] 0.9 0.5 0.1

..$ hyper : num [1:5] 0.9 0.5 0.075 0.3 -0.25

..$ tuning : num 0.03

..$ sigma_MH: num [1:2, 1:2] 1 -0.25 -0.25 1

..$ npart : num 10

..$ mcmseed : num 90210

💡 And as always, references and details are in the help file (?SV.mcmc). The techniques are not covered in tsa4.

Classical:

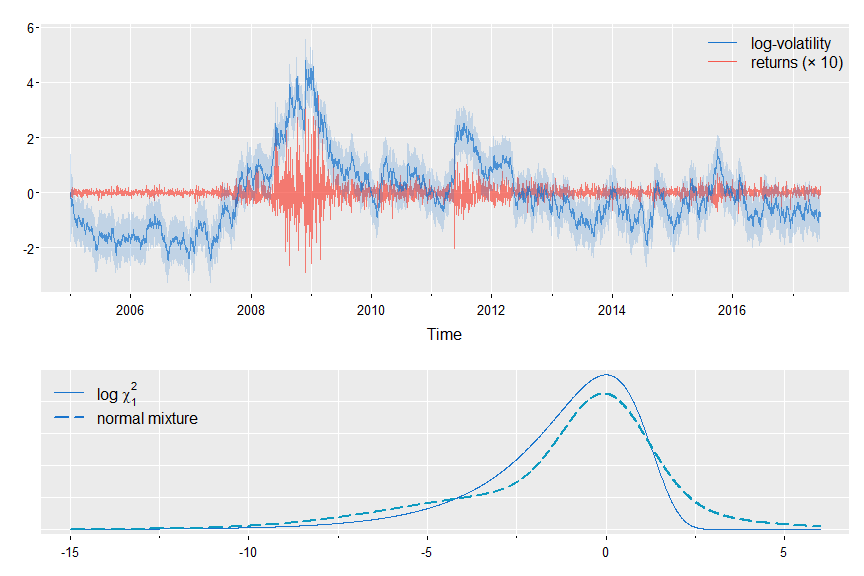

🦄 We’ll fit an SV model with feedback (aka leverage) to the daily returns of Bank of America (in astsa). The returns are $r_t$ and the log volatility is $x_t = \log \sigma_t^2$ with \(x_{t+1} = \gamma r_t + \phi x_t + \sigma w_t.\) The prior return feeds back directly into the volatility. The observations are $y_t = \log r_t^2$, and \(y_t = \alpha + x_t + \eta_t\) where $\eta_t$ is a mixture of two normals, one centered at zero.

More details are in the text (obviously). You can have $\text{corr}(w_t, \eta_t) = \rho$, but it’s not needed if you include feedback.

SV.mle(BCJ[,'boa'], feedback=TRUE, rho=0) # rho not included if no start value given

Coefficients:

gamma phi sQ alpha sigv0 mu1 sigv1 rho

estimates -1.9464 0.9967 0.1260 -8.5394 1.1997 -2.1895 3.6221 0.1982

SE 0.5063 0.0023 0.0266 0.7049 0.0509 0.1778 0.1085 0.3970

Notice that $\rho$ is not significant and its SE is huge! And you get a graphic of the predicted $x_t$ superimpose on $r_t$ (times 10), and a comparison of the distribution of $\eta_t$ vs $\log \chi_1^2$,

To do the same run but without $\rho$, just don’t give it an initial value:

SV.mle(BCJ[,'boa'], feedback=TRUE)

# and output (the graphics are nearly the same so it's a no show)

Coefficients:

gamma phi sQ alpha sigv0 mu1 sigv1

estimates -1.9514 0.9968 0.1287 -8.5241 1.1925 -2.1916 3.6965

SE 0.5029 0.0023 0.0267 0.7215 0.0455 0.1806 0.1083

and to ignore the feedback term, just leave it out of the call (but why would you?): SV.mle(BCJ[,'boa'])

12. Arithmetic

💡 The package has a few scripts to help with items related to time series and stochastic processes.

ARMAtoAR

🔵 R stats has an ARMAtoMA script to help visualize the causal form of a model. To help visualize the invertible form of a model, astsa includes an ARMAtoAR script. For example,

# ARMA(2, 2) in causal form [rounded for your pleasure]

ARMAtoMA(ar = c(1.5, -.75), ma = c(-.8,.4), 50)

[1] 0.7000 0.7000 0.5250 0.2625 0.0000 -0.1969 -0.2953 -0.2953 -0.2215 -0.1107

[11] 0.0000 0.0831 0.1246 0.1246 0.0934 0.0467 0.0000 -0.0350 -0.0526 -0.0526 ...

giving some of the ψ-weights in the xt = ∑ψj wt-j representation of the model (wt is white noise). If you want to go the other way, use

# ARMA(2, 2) in invertible form [rounded for your pleasure]

ARMAtoAR(ar = c(1.5, -.75), ma = c(-.8,.4), 50)

[1] -0.7000 -0.2100 0.1120 0.1736 0.0941 0.0058 -0.0330 -0.0287 -0.0098 0.0037

[11] 0.0068 0.0040 0.0005 -0.0012 -0.0012 -0.0004 0.0001 0.0003 0.0002 0.0000 ...

giving some of the π-weights in the wt = ∑πj xt-j representation of the model.

💡 As a side note, you can check if a model is causal and invertible using arma.spec() from astsa, and if you’re not careful

arma.spec(ar = c(1.5, -.75), ma = c(-.8,-.4))

WARNING: Model Not Invertible

Error in arma.spec(ar = c(1.5, -0.75), ma = c(-0.8, -0.4)) : Try Again

Matrix Powers

🔵 We compute Σ -½ where Σ is a variance-covariance matrix when calculating the spectral envelope. Also, the square root of a covariance matrix can be useful for state space modeling via Kfilter, Ksmooth, and EM.

So, we built in a script called matrixpwr that computes powers of a square matrix, including negative powers for nonsingular matrices.

Also, %^% is available as a more intuitive operator. For example,

var(econ5)%^%-.5 # rounded here (not by the script) for you pleasure

[,1] [,2] [,3] [,4] [,5]

[1,] 1.073 0.005 -0.017 0.006 0.021

[2,] 0.005 0.017 -0.019 -0.009 -0.010

[3,] -0.017 -0.019 0.026 0.006 0.004

[4,] 0.006 -0.009 0.006 0.025 0.006

[5,] 0.021 -0.010 0.004 0.006 0.033

where

round(var(econ5), 1)

unemp gnp consum govinv prinv

unemp 2.9 782.4 565.4 117.4 114.2

gnp 782.4 661297.3 449876.0 111333.5 117830.4

consum 565.4 449876.0 307483.0 74977.9 79860.3

govinv 117.4 111333.5 74977.9 20780.9 19381.8

prinv 114.2 117830.4 79860.3 19381.8 22126.5

🔵 But also, if you’re playing with Markov Chains, you can learn about long run distributions by raising the transition matrix to a large power. Here’s a demonstration of convergence in a 2 state MC:

( P = matrix(c(.7,.5,.3,.5), 2) ) # 1 step transitions

[,1] [,2]

[1,] 0.7 0.3

[2,] 0.5 0.5

( P %^% 5 ) # 5 step transitions

[,1] [,2]

[1,] 0.62512 0.37488

[2,] 0.62480 0.37520

( P %^% 50 ) # 50 step transitions

[,1] [,2]

[1,] 0.625 0.375

[2,] 0.625 0.375

π(1) = 5/(3+5) = .625 and π(2) = 3/(3+5)=.375 and almost there in 5 steps.

A note - if you use it in an expression, surround the operation with parentheses:

c(.5,.5) %*% ( P %^% 50 ) # toss a coin for initial state

[,1] [,2]

[1,] 0.625 0.375

# but this draws an error because %*% is first

c(.5,.5) %*% P %^% 50

Polynomial Multiplication

🔵 The script sarima.sim uses polyMul when simulating data from seasonal ARIMA models.

For example,

(1 - 1.5B1 + .75B2)×(1 - .9B12) xt =wt

which is an ARIMA(2,0,0)×(1,0,0)12 model. You can add MA and SMA parts to your liking in the same manner. Here’s the AR polynomial on the left (ARpoly) and then the AR coefficients when on the right (ARparm):

ar = c(1, -1.5, .75)

sar = c(1, rep(0,11), -.9)

AR = polyMul(ar,sar)

( ARpoly = cbind(order=0:14, ARpoly=AR) )

order ARpoly

[1,] 0 1.000

[2,] 1 -1.500

[3,] 2 0.750

[4,] 3 0.000

[5,] 4 0.000

[6,] 5 0.000

[7,] 6 0.000

[8,] 7 0.000

[9,] 8 0.000

[10,] 9 0.000

[11,] 10 0.000

[12,] 11 0.000

[13,] 12 -0.900

[14,] 13 1.350

[15,] 14 -0.675

which is xt -1.5 xt-1 +.75 xt-2 - .9 xt-12 + 1.35 xt-13 - .675 xt-14 = wt , or

( ARparm = cbind(order=1:14, ARparm=-AR[-1]) )

order ARparm

[1,] 1 1.500

[2,] 2 -0.750

[3,] 3 0.000

[4,] 4 0.000

[5,] 5 0.000

[6,] 6 0.000

[7,] 7 0.000

[8,] 8 0.000

[9,] 9 0.000

[10,] 10 0.000

[11,] 11 0.000

[12,] 12 0.900

[13,] 13 -1.350

[14,] 14 0.675

which is xt = 1.5 xt-1 -.75 xt-2 + .9 xt-12 -1.35 xt-13 + .675 xt-14 + wt .

🤡 That was fun!

13. The Spectral Envelope

DNA and the Spectral Envelope

💡 There are 2 scripts to accomplish spectral analysis of DNA sequences,

specenvanddna2vector

and then there are a few data files,

bnrf1ebv,bnrf1hvs, andEBV.

🔵 The first and second files are the nucleotide sequence of the BNRF1 gene (3741 bp) of the Epstein-Barr virus (EBV) and of the herpesvirus saimiri (HVS) using the coding 1=A, 2=C, 3=G, 4=T. EBV is the FASTA file of the entire Epstein-Barr virus sequence taken from NCBI, 172281 bp. It’s not useful on its own, but using dna2vector, different regions can be explored. For example,

# EBV looks like "AGAATTCGTCTTG ...", one very long string

ebv = dna2vector(EBV)

head(ebv)

[,1] [,2] [,3] [,4]

[1,] 1 0 0 0

[2,] 0 0 1 0

[3,] 1 0 0 0

[4,] 1 0 0 0

[5,] 0 0 0 1

[6,] 0 0 0 1

🔵 To use specenv, the input sequence has to be a matrix of indicators like the output above. That’s where dna2vector comes in. There are many examples in the help file (?dna2vector), but here’s a few to whet the appetite.

🟪 Let’s say you download a DNA sequence as a FASTA file called sequence.fasta.

It will look something like this:

>HSBGPG Human gene for bone gla protein (BGP)

GGCAGATTCCCCCTAGACCCGCCCGCACCATGGTCAGGCATGCCCCTCCTCATCGCTGGGCACAGCCCAGAGGGT

ATAAACAGTGCTGGAGGCTGGCGGGGCAGGCCAGCTGAGTCCTGAGCAGCAGCCCAGCGCAGCCACCGAGACACC

ATGAGAGCCCTCACACTCCTCGCCCTATTGGCCCTGGCCGCACTTTGCATCGCTGGCCAGGCAGGTGAGTGCCCC

If the file is in the working directory, the following code can be used to read the data into the session, create the indicator sequence and save it as a compressed R data file:

fileName <- 'sequence.fasta' # name of FASTA file

data <- readChar(fileName, file.info(fileName)$size) # input the sequence

bone <- dna2vector(data) # convert it to indicators

save(bone, file='bone.rda') # save the file as a compressed file

load('bone.rda') # and load 'bone' when you need it

🟪 Here are some other examples using dna2vector, which takes two arguments,

data and alphabet. Of course data is the object that contains the sequence data, and alphabet is the particular alphabet used in the file, which defaults to ` alphabet = c(“A”, “C”, “G”, “T”) for strings and alphabet = 1:4 for numeric data such as bnrf1ebv`.

####################################################################

## gene BNRF1 of EBV with 1, 2, 3, 4 for "A", "C", "G", "T" ##

## remember 'bnrf1ebv' is a data set in astsa and it is a numeric ##

####################################################################

xdata = dna2vector(bnrf1ebv)

# note:

head(bnrf1ebv)

[1] 1 4 3 3 1

# and

head(xdata)

[,1] [,2] [,3] [,4]

[1,] 1 0 0 0

[2,] 0 0 0 1

[3,] 0 0 1 0

[4,] 0 0 1 0

[5,] 1 0 0 0

##########################

## raw GenBank sequence ##

##########################

data <-

c("1 agaattcgtc ttgctctatt cacccttact tttcttcttg cccgttctct ttcttagtat

61 gaatccagta tgcctgcctg taattgttgc gccctacctc ttttggctgg cggctattgc")

xdata = dna2vector(data, alphabet=c('a', 'c', 'g', 't'))

head(xdata)

[,1] [,2] [,3] [,4]

[1,] 1 0 0 0

[2,] 0 0 1 0

[3,] 1 0 0 0

[4,] 1 0 0 0

[5,] 0 0 0 1

##########################

## raw FASTA sequence ##

##########################

data <-

c("AGAATTCGTCTTGCTCTATTCACCCTTACTTTTCTTCTTGCCCGTTCTCTTTCTTAGTATGAATCCAGTA

TGCCTGCCTGTAATTGTTGCGCCCTACCTCTTTTGGCTGGCGGCTATTGCCGCCTCGTGTTTCACGGCCT")

xdata = dna2vector(data)

head(xdata)

[,1] [,2] [,3] [,4]

[1,] 1 0 0 0

[2,] 0 0 1 0

[3,] 1 0 0 0

[4,] 1 0 0 0

[5,] 0 0 0 1

💡 specenv calculates the spectral envelope defined in the original paper, summarized in Statistical Science and discussed in Chapter 7 of the text.

By default, it produces a graph of the spectral envelope and an approximate significance threshold and invisibly return a matrix containing: frequency, spectral envelope ordinates, and scaling of the categories in the order of the categories in the alphabet.

🟪 A very simple run is something like this

xdata = dna2vector(bnrf1ebv)

u = specenv(xdata, spans=c(7,7)) # graphic below

head(u) # output - coefs are scalings in order of 'alphabet' (A C G T here)

freq specenv coef[1] coef[2] coef[3] coef[4]

[1,] 0.00025 0.002034738 -0.5014652 -0.5595067 -0.6599128 0

[2,] 0.00050 0.001929567 -0.5162806 -0.5557567 -0.6516047 0

[3,] 0.00075 0.001747429 -0.5402356 -0.5498484 -0.6370339 0

[4,] 0.00100 0.001587832 -0.5716387 -0.5398917 -0.6178560 0

[5,] 0.00125 0.001511232 -0.6025964 -0.5307763 -0.5959481 0

🟪 One more example… you can specify a section (section = start:end) to work on and the significance threshold (or turn it off significance = NA), plus other options.

Here’s one for a section of the EBV.

xdata = dna2vector(EBV)

u = specenv(xdata, spans=c(7,7), section=50000:52000) # repeat section

round(head(u), 3) # output

freq specenv coef[1] coef[2] coef[3] coef[4]

[1,] 0.000 0.055 0.520 -0.529 -0.671 0

[2,] 0.001 0.047 0.519 -0.531 -0.671 0

[3,] 0.001 0.037 0.514 -0.536 -0.669 0

[4,] 0.002 0.026 0.507 -0.547 -0.667 0

[5,] 0.002 0.017 0.493 -0.564 -0.662 0

Optimal Transformations and the Spectral Envelope

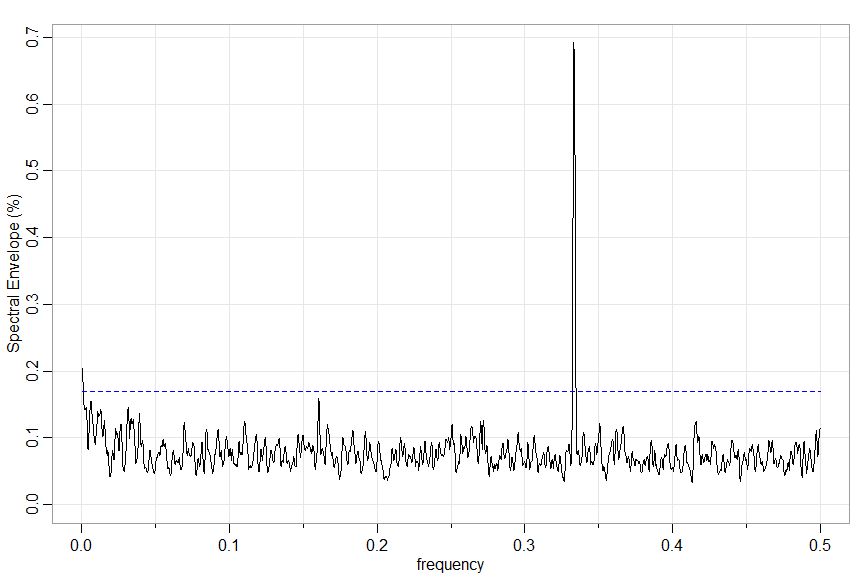

The script

specenv()

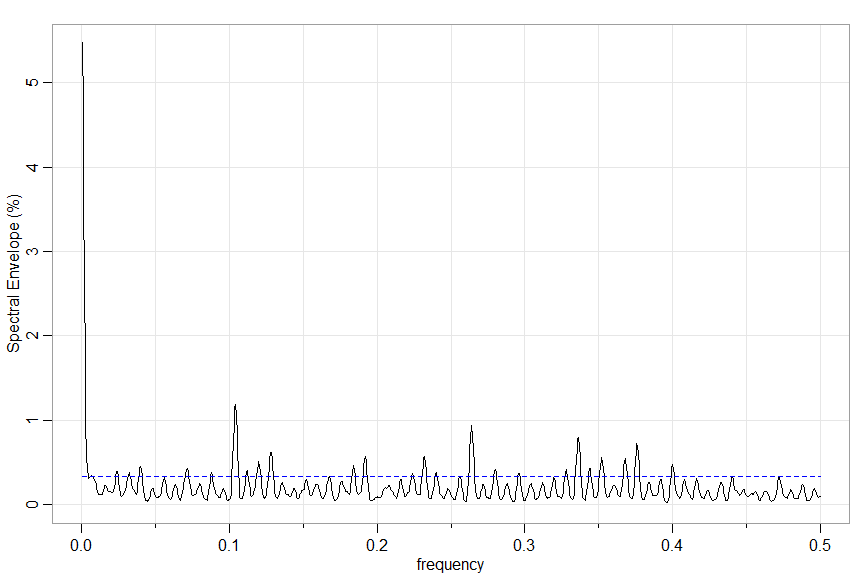

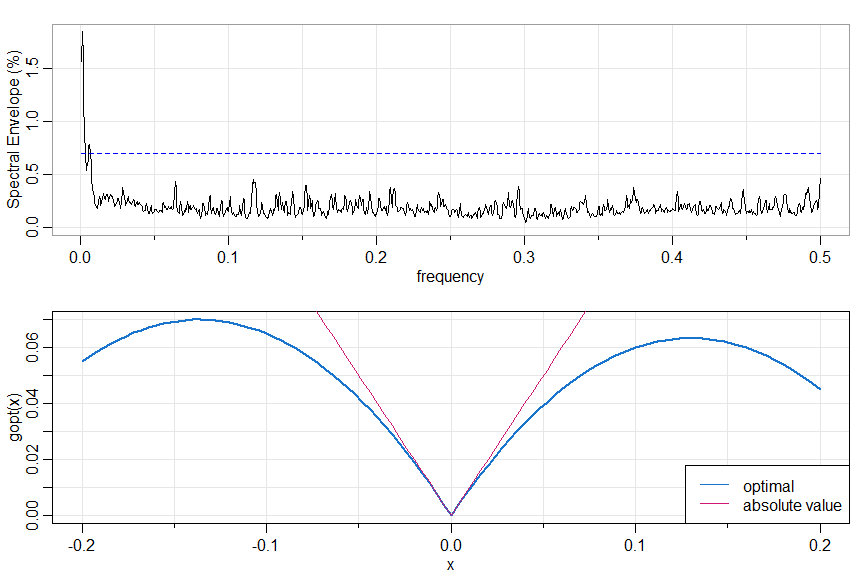

can also be used to find optimal transformations of real-valued time series. For example, we’ve seen the NYSE returns are nonlinear.

x = astsa::nyse

# possible transformations include absolute value and squared value

xdata = cbind(x, abs(x), x^2)

par(mfrow=2:1)

u = specenv(xdata, real=TRUE, spans=c(3,3))

# peak at freq = .001 so let's

# plot the optimal transform

beta = u[2, 3:5] # scalings

b = beta/beta[2] # makes abs(x) coef=1

gopt = function(x) { b[1]*x+b[2]*abs(x)+b[3]*x^2 }

curve(gopt, -.2, .2, col=4, lwd=2, panel.first=Grid(nym=0))

gabs = function(x) { b[2]*abs(x) } # corresponding to |x|

curve(gabs, -.2, .2, add=TRUE, col=6)

legend('bottomright', lty=1, col=c(4,6), legend=c('optimal', 'absolute value'), bg='white')

🙈 🙉 🙊 THAT’S A WRAP 🙊 🙉 🙈